%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsSeptember 2025 - Market Update

- The Federal Reserve bank lowered its target rate by 25bps, cutting rates for the first time since 2024.

- US large cap stocks reached record highs, returning 3.64% for the month of September.

- Job growth slowed and consumer spending remained resilient as the US federal government headed towards an October shutdown.

- Big Tech and consequently Large Cap stocks outperformed Mid and Small cap stocks in September.

- Gold reached all-time highs, surging 11.78% in September, as investors kept pouring money into the safe haven.

Data Dashboard

Stock Market

AI investment momentum kept building, and Technology continued to be the dominant sector throughout September. The S&P 500 now trades at 23 times forward earnings, almost 20% higher than the 10-year average. Technology was the best performing sector, driven by a series of high-profile contracts announced by ChatGPT developer OpenAI, with Oracle, Microsoft and Nvidia. Growth and momentum are still the key driving factors behind equity returns.

Small Cap stocks returned 12.4% in Q3 compared to 8.1% for Large Cap stocks, and stand at an average P/E ratio of 16x, which could offer more upside potential.

September Monthly Returns (by GICS Sector)

Bond Market

The Federal Reserve announced a long anticipated rate cut in September, citing weakness in US jobs data. The US Aggregate bond index outperformed the global aggregate bond index in September. History shows that bonds tend to benefit from Fed easing, while equity performance is a little more varied. There have been 5 distinct Fed rate cut cycles since 1989, and every cycle (even ones with long pauses) has been positive for bonds.

The US Corporate High Yield average spread (the difference in yield between junk bonds and US treasuries) is at 2.65%, looming near 10 year lows. This tells us a compelling story—investors are not willing to pay much of a premium to hold onto credit risk over US Treasurys.

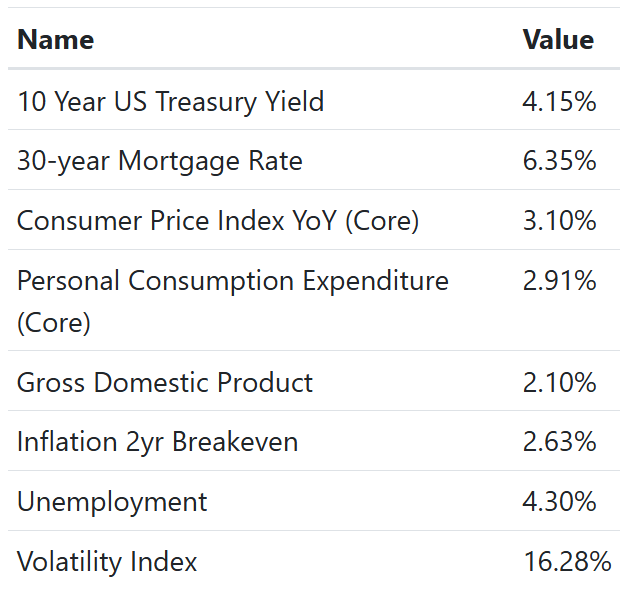

The 10Y Treasury yield dipped a little and is presently hovering around 4.15%.

Investors should watch out for developments into October and how the Federal Reserve provides insights into the economy, especially considering the lack of office economic data releases.

Economics

Real GDP accelerated at a 3.8% annualized pace in Q2 2025, rebounding from a -0.6% contraction in Q1. The Q2 strength was led by consumer spending (and a drag from fewer imports), confirming a mid-year re-acceleration heading into Q3.

Official September data is going to be delayed by the U.S. government shutdown, which has paused BLS/BEA releases (including the September jobs report and CPI). Several private proxies point to softer hiring momentum in September while we await the official releases. Uncertainty is heightened with the shutdown, exacerbated by the White House potentially threatening to fire thousands of federal workers, and axing "democrat" agencies.

Available August reads showed consumers still spending: retail sales rose +0.6% m/m and +5.0% y/y, while PCE inflation firmed to 2.7% y/y (core details mixed). Services activity cooled, with ISM Services at 50.0 and manufacturing new orders slipped back into contraction.

Mortgage costs eased into late September: the 30-yr Freddie Mac PMMS rate printed 6.26% (Sep 18) and 6.30% (Sep 25), before ticking to 6.34% on Oct 2—still below the 52-week average. Markets are heavily priced for another 25 bps Fed cut at the Oct 28–29 FOMC (~96.7% odds per swaps markets), even as some Fed officials push back on aggressive easing.

Gold and Silver have repeatedly breached all-time highs to return 45% and 58% YTD, as investors keep pouring money into the safe havens in the wake of a government shutdown, steady inflation, slowing job markets and persistent global political crises.

September Economic Dashboard

Portfolio Changes

Our tactical ETF portfolio saw a rotation back into Gold Miners amidst rising policy uncertainty and a volatile US dollar. In the low volatility portfolio, we have increased credit exposure and added mortgages.

Rebalancing remains a core pillar of our strategy—trim outsized winners back to target, and add selectively to underweights. We recommend staying diversified as the S&P gets top-heavier, to keep exposure beyond mega-cap tech.

As always, please feel free to reach out with any questions or concerns.

Thanks,

The Friedenthal Financial Team