%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsOctober 2025 - Market Update

- Mega-cap/AI leadership lifted broad U.S. equities with Technology leading sector returns.

- Defensive sectors (Health Care, Utilities) outperformed while cyclicals were mixed.

- Treasury yields hovered slightly lower than in September after the Federal Reserve cut its benchmark borrowing rate by 25bps at their October FOMC meeting.

- Economic warning signs are growing despite record markets and steady unemployment.

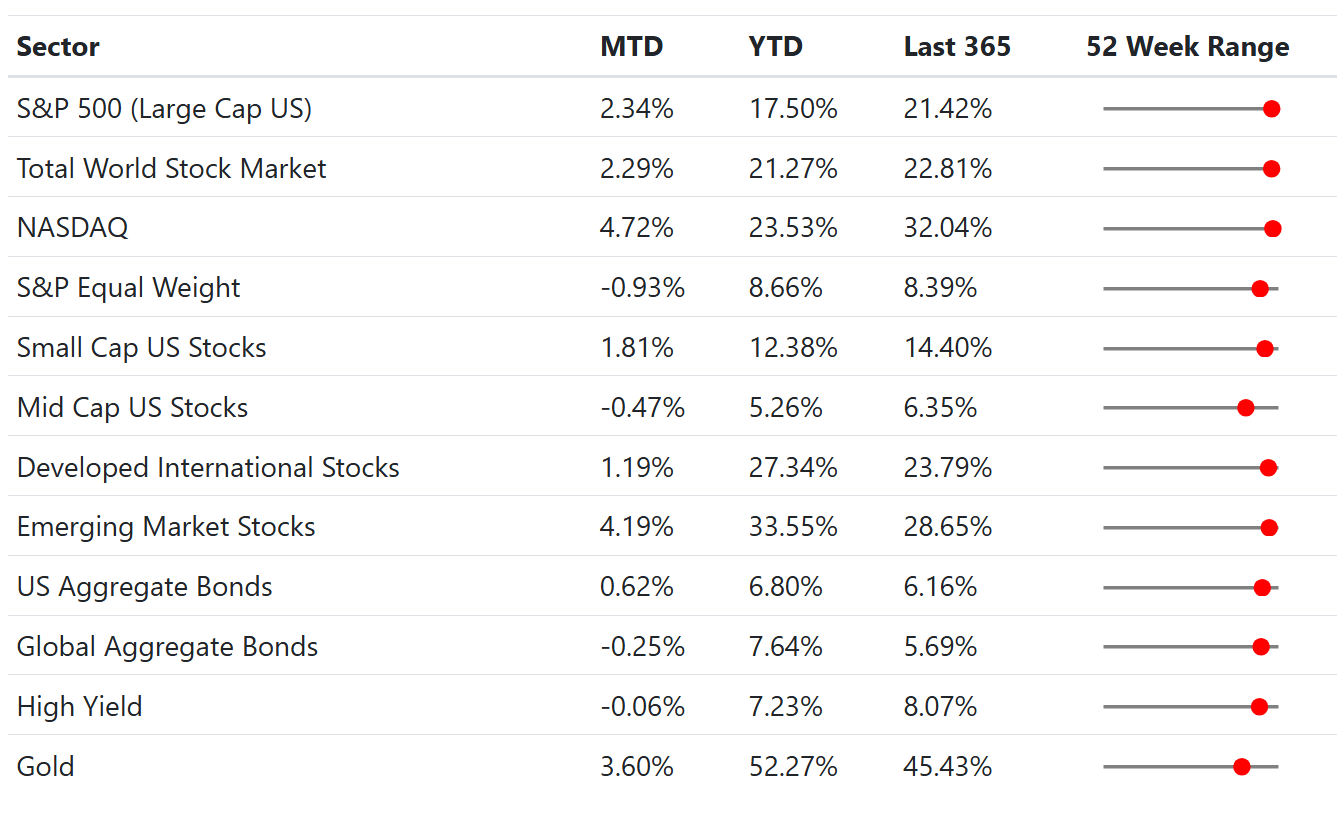

Data Dashboard

Stock Market

Market Cap weighted indices benefited from concentrated leadership in Mega-Cap technology while equal-weight lagged. This is classic late-cycle behavior when investors prize perceived quality, earnings visibility, and balance-sheet strength. Defensive sectors such as Health Care and Utilities outperformed most cyclicals. Utilities have received tailwinds from the AI theme, due to increased energy demand.

Valuations in the leaders remain above long-run averages in our view, which argues for balance across styles and sectors. Wall Street has argued more recently that a short-term pullback could be healthy for markets, notwithstanding bullish long-term expectations. Credit headlines briefly added caution. The bankruptcy of First Brands—an auto-parts supplier undergoing restructuring—rekindled questions about pockets of credit quality and controls. While we did not see broad contagion, episodes like this can momentarily pressure lower-quality issuers and funding costs before markets refocus on fundamentals.

In recent months we’ve seen a noteworthy ripple effect emanating from OpenAI’s infrastructure and partnership ecosystem. For example, chip-maker AMD announced a strategic agreement with OpenAI involving up to 6 gigawatts of next-gen GPU deployments and a warrant granting OpenAI the option to acquire up to 160 million shares of AMD common stock — a clear signal of mutual incentives and alignment. Meanwhile, cloud-giant Amazon Web Services (AWS) revealed a multi-year partnership with OpenAI worth roughly $38 billion, which helped drive Amazon’s stock to record highs. And although OpenAI itself remains privately held, the announcement that Microsoft Corporation will hold roughly a 27% stake (valued at about $135 billion) in OpenAI’s for-profit arm bolstered investor sentiment toward Microsoft’s AI positioning.

For investors, this ecosystem effect means that companies upstream and downstream of OpenAI are gaining visibility — not merely as hardware or cloud vendors, but as strategic collaborators whose fortunes become more tightly linked to the broader AI build-out. We believe this dynamic helps explain why so many technology and infrastructure names have responded positively to OpenAI-related announcements, and why the AI narrative continues to have meaningful weight even in a market environment where breadth remains narrow. However, investors should remain cautious as this kind of an effect has a tendency to elevate lofty valuations, as more and more investors start to experience FOMO and chase trends. Its important to keep level-headed and have a viable and consistent long-term investing strategy that we can stick with in both up and downturns.

October Return Summary (by GICS Sector)

Bond Market

After the 25 bps FOMC cut on October 29, rates traded in a relatively contained range through the first days of November, with the 10-year near our dashboard print. High-yield spreads (the extra yield over Treasurys) were broadly steady, reflecting a still-constructive risk backdrop even as idiosyncratic credit stories surfaced. In this environment, we believe balance matters: modest, diversified duration, with a quality tilt in credit to help buffer bouts of volatility tied to shifting policy odds.

Economics

Inflation continues to cool at the margin: Core CPI came in at 3% YOY and Core PCE at 2.91%. GDP growth was at 2.10%, while the unemployment rate came in at 4.30%. While these numbers suggest cooling prices and a growing economy, a report by JP Morgan suggests that 1.1% of the GDP growth in the first half of 2025 was driven just by AI related capital expenditures.

The 30-year fixed mortgage rate (national average) is hovering around 6.25%, and the 2-year breakeven rate for TIPS (Treasury Inflation Protected Securities) is at 2.60%. The VIX Index at 17.44 suggests contained—but not complacent—volatility. We view this mix as consistent with slower growth and more two-way market days.

Policy and fiscal backdrop: the ongoing federal government shutdown has disrupted services and delayed some payments. A visible flashpoint has been SNAP (food assistance)—with partial/paused November funding and legal back-and-forth creating uncertainty for millions of households. That can dampen near-term consumption at the margin, particularly for retailers serving lower-income customers, while the broader GDP effect depends on the shutdown’s duration.

Precious metals & sentiment: After October’s record highs in gold and silver, November saw periods of consolidation as the dollar firmed; investors continue to use metals as a hedge against policy and geopolitical risk. Silver’s rally has been more volatile than gold’s—typical given its smaller market and industrial exposure—so pullbacks can be sharper even when long-term drivers remain supportive.

What we’re watching: newly announced corporate layoffs (from large tech/industrial names to select financials) that can influence confidence and spending; and an active early-November earnings slate (e.g., AMD, Palantir, Uber, BP, Novo Nordisk, AstraZeneca, ConocoPhillips) that may steer sector leadership into year-end.

October Economic Dashboard

Portfolio Changes

In our tactical ETF portfolio, we rotated out of our Uranium (URA) ETF (which has performed spectacularly), and moved into Lithium. We also invested in Biotech, while eliminating our position in Homebuilders.

In our low-volatility tactical portfolio, we have been maintaining some exposure in either US dollar-denominated or local-currency foreign bonds. We also retain our portfolio view of low to intermediate duration & higher credit tilt, compared to the US Aggregate Bond index.

As always, please feel free to reach out with any questions or concerns.

Thanks,

The Friedenthal Financial Team