%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsNovember 2025 - Market Update

- Equities rallied into month-end on rising expectations of a December Fed rate cut, with small-caps outperforming large caps as easing financial conditions were priced in.

- Tech leadership shifted sharply as AI-driven volatility hit high-valuation names—Nvidia slumped while Alphabet surged—producing a more mixed sector backdrop.

- Defensive sectors and international markets held firm, with Health Care leading US sectors and Europe benefiting from increased defense spending, while EM equities softened due to Asia’s tech weakness.

- Bond yields drifted lower and economic data stayed mixed, with cooling inflation and steady credit markets alongside strong jobless-claims data but rising corporate layoff announcements.

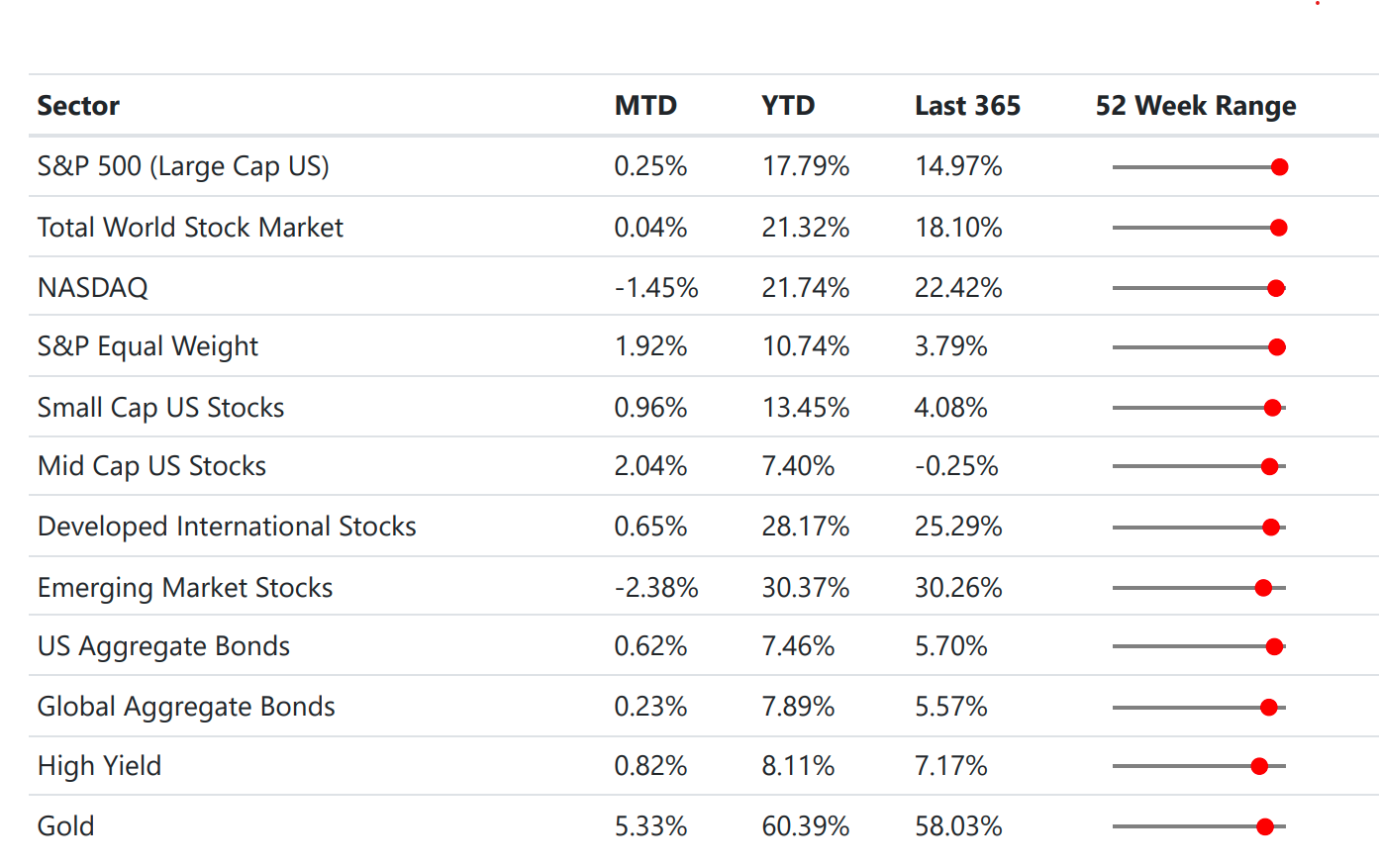

Data Dashboard

Stock Market

US equities managed a modest gain for November, overcoming a mid-month stumble to end on a high note. The S&P 500 rose about +0.3% for the month, and the Dow Jones index also notched a monthly gain. In contrast, the tech-heavy Nasdaq 100 fell 1.6%, snapping a seven-month winning streak. A significant factor was the volatility in superstar tech stocks: Nvidia's 12.6% plunge in November erased some of its year-to-date gains, as investors rotated out of crowded AI trades. On the flip side, Alphabet’s stock soared to record highs on a 13.6% monthly jump, driven by a 34% surge in Google Cloud revenue and new AI initiatives, which attracted capital away from chipmakers toward software and services. This intra-tech rotation – essentially a leadership handoff from semiconductor names to cloud and platform companies – broadened market participation.

It also highlights a late-cycle dynamic: investors growing choosier within the tech/AI theme, rewarding fundamentally strong firms while punishing those seen as overvalued. Meanwhile, November’s final week brought a broad relief rally after Thanksgiving, as growing conviction in a December Fed rate cut lifted sentiment across the board. Small-cap stocks, being more sensitive to credit conditions, outpaced large-caps in November.

Beneath the surface, sector leadership underwent a notable shift. After many months of mega-cap dominance, defensive and value-oriented sectors took the lead in November. Health Care in particular extended its resurgence – it was the top-performing sector over the past four months, gaining over 9% for the month. Other traditionally defensive sectors like Consumer Staples and even Energy (helped by stabilizing oil prices and dividend appeal) provided support. In contrast, “momentum” stocks saw a pullback as the AI hype moderated and questions arose about monetization timelines for new innovations. This rotation to defensives suggests that investors sought quality and earnings visibility amid November’s volatility. Encouragingly, corporate fundamentals remained solid: with about 95% of S&P 500 companies reporting third-quarter results, earnings growth came in stronger than expected (average revenues 8.4%year-over-year, the best since 2022) and many firms continued stock buybacks. Those robust results and shareholder returns helped cushion the market during bouts of weaker sentiment.

Overall, the stock market’s internals in November paint a picture of a maturing rally—one still underpinned by decent earnings, but rotating in character. We continue to emphasize balance and discipline, as periods of AI-driven euphoria can quickly correct. Maintaining a diversified long-term strategy is crucial to navigate both the surges and pullbacks.

Looking abroad, international equities were mixed but generally resilient. Developed market stocks edged higher, bolstered by Europe’s stimulus efforts and increased defense spending amid ongoing geopolitical conflicts. In contrast, emerging market (EM) equities saw their first notable stumble in months, as the same high-flying tech theme took a breather globally. Key emerging markets like South Korea and Taiwan, home to major semiconductor and tech hardware firms, were notable laggards, with those indices down sharply in November. This was partly a reaction to lofty valuations and some profit-taking after outsized year-to-date gains. Even so, emerging markets remain up roughly 30% in 2025 and on track for their best year since 2017.

November Return Summary (by GICS Sector)

Bond Market

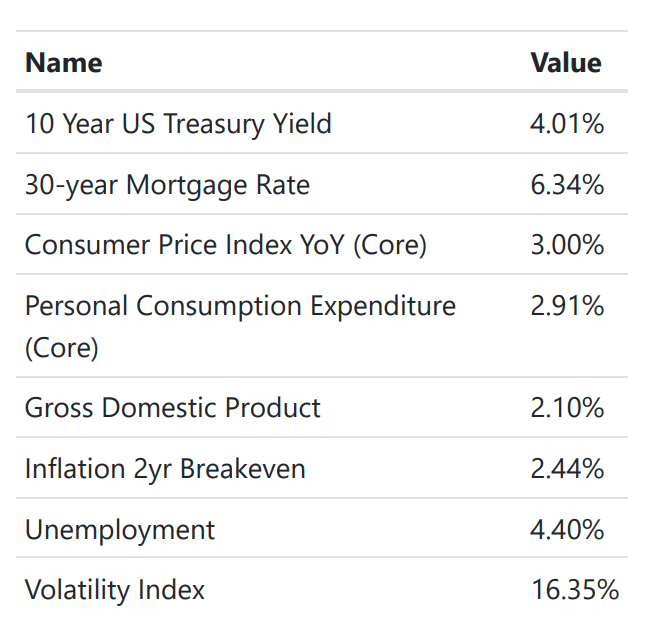

Bonds provided stability in portfolios during November’s equity gyrations. The US bond market posted modest positive returns for the month, as interest rates drifted slightly lower. The benchmark 10-year Treasury yield ended November around 4.0%, down from ~4.11% at October’s close. This gentle decline in yields reflected a mix of limited economic data (due to the federal shutdown) and increasing confidence that the Fed’s next move will be rate cuts rather than hikes. In fact, Treasury yields traded in a relatively narrow range for most of the month. Short-term rates like the 2-year Treasury fell a bit more than long rates, steepening the yield curve slightly off its most inverted levels as markets priced in potential 2026 easing. High-quality bonds benefited from this environment: the broad Bloomberg US Aggregate Bond Index rose 0.6% in November.

Within fixed income, corporate bonds outperformed government bonds in November. Investment-grade corporate bond indices gained roughly 0.7%, slightly ahead of Treasuries. This outperformance came even as credit spreads widened just a touch – the extra yield premium on corporate debt over Treasuries ticked up – because the overall yield level on corporate bonds is higher, providing better income cushion. Investors continued to gravitate toward the reliable income from corporate and high-quality securitized bonds, given that yields remain historically elevated. Notably, high-yield (“junk”) bonds were relatively steady; spreads in that segment held broadly unchanged, indicating that investors are not (yet)signaling significant stress in lower-quality credit.

Economics

The macroeconomic backdrop in late 2025 presents a mix of encouraging progress and lingering concerns. On the positive side, inflation has been steadily cooling. The latest readings show core inflation hovering around the 3% YoY mark, the lowest in over two years. This is a significant decline from the peak inflation rates seen in 2022, bringing price increases much closer to the Fed’s 2% target. Easing price pressures have been helped by improving supply chains and the impact of the Fed’s earlier rate hikes, and they give the Fed scope to consider policy easing. Economic growth, meanwhile, has been positive but moderating. US GDP grew at an annualized 2.1% pace in the third quarter, a slight comedown from the first half’s rapid growth.

Consumer spending has remained resilient overall (aided by a strong labor market and excess savings), yet higher borrowing costs are weighing on interest-sensitive sectors like housing. Globally, other major economies are also experiencing cooler inflation and mixed growth. Europe is grappling with high energy costs but benefiting from fiscal stimulus, and China’s growth has been uneven as policymakers there provide selective support. Economic data suggest a transition to a late-cycle phase of slower, more sustainable growth with declining inflation, which is essentially what the Fed has been trying to engineer.

The labor market is a key focal point, sending some conflicting signals. Official US employment data for November was delayed by the government shutdown and will only be released in mid-December. However, alternative indicators painted a nuanced picture. On one hand, seasonally adjusted initial jobless claims plunged to just 191,000 at the end of November, the lowest level of new claims since September 2022. Similarly, the unemployment rate (last seen at 4.3% in October) likely remained low by historical standards. On the other hand, announced corporate layoffs have been making headlines.

The tech sector in particular has seen a wave of redundancies as companies streamline and adopt efficiency gains from AI integrations. Notably, though, the pace of new layoff announcements slowed in November (planned job cuts for the month were down 53% from October). This suggests a bifurcated labor market: large tech and industrial firms are trimming excess roles after years of expansion, even as smaller businesses still struggle to hire workers in a tight pool. Wage growth has also cooled somewhat but remains positive, helping consumers keep up with the cost of living as inflation abates. Our interpretation is that the labor market is loosening at the margins – we’re past the breakneck pace of job growth – but it is still far from any kind of severe downturn.

Economic Dashboard

Portfolio Changes

In our tactical ETF portfolio, we added clean energy and semiconductors, while rotating out of our China and Aerospace/Defense positions.

In out tactical low-volatility portfolio, we increased duration and added to more sovereign debt, both US govt and foreign USD denominated bonds. We also reduced credit exposure, switching out of convertibles in favor of senior loans.

What to Watch Going into December

- Federal Reserve December Meeting (Dec 9–10): The Fed’s final policy meeting of 2025 is the centerpiece for markets. Expectations are high that the Fed will cut interest rates by 0.25% at this meeting – futures are pricing in roughly an 80–85% probability of a cut. This would follow the 25 bps cut implemented in October. Investors will be watching not just the decision itself, but also the Fed’s tone on future rate moves. Any guidance on the pace of rate cuts in 2026 (or conversely, hesitation due to still-above-target inflation) could swing both bond and stock markets. Fed Chair Powell’s press conference will be scrutinized for how confident the Fed is that inflation will stay subdued if they begin easing. A rate cut in December is largely seen as a positive catalyst by equity markets, but if the Fed surprises (for example, if they leave rates unchanged or sound more hawkish than expected), we could see volatility pick up.

- Delayed US Employment Report: Because of the earlier data blackout, the official November jobs report will arrive mid-December. This release will be important to confirm what earlier hints suggested: did the economy add jobs or lose jobs in November?

- Holiday Shopping and Consumer Health: : As we enter the critical holiday season, consumer spending trends will be a key gauge of economic momentum. Early reports from Black Friday and Cyber Monday indicated solid, though not spectacular, sales growth. So far, low unemployment and rising real wages (with inflation lower) have supported consumption, but high interest rates and depleted savings could lead to more frugal holiday behavior. Sectors like e-commerce and consumer electronics will give insight into discretionary spending appetite.

As we wrap up 2025, feel free to reach out with any questions about IRA distributions (including RMDs), taxes, year-end tax-loss harvesting, or even exploring whether a December Roth conversion might make sense for you.

Thanks,

The Friedenthal Financial Team