%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsMay 2026 - Market Recap

- U.S. stocks extended their rally, with the S&P 500 gaining 5.26% in May and closing the month at fresh record highs. It was the index's second straight positive month, powered by a sharp comeback in MegaCap technology and a cooling of the energy shock that had rattled markets earlier in the year.

- Oil prices fell roughly 19% during the month — Brent crude's worst month since the pandemic, as the US and Iran moved toward ceasefire negotiations and markets priced out the worst-case scenario for the Strait of Hormuz. The relief flowed straight through to inflation expectations and risk appetite.

- Technology led decisively while Energy lagged, a near-complete reversal of the prior few months. Nvidia's blowout quarterly results and renewed enthusiasm for AI infrastructure spending anchored the move.

- Leadership at the Federal Reserve changed hands. The Senate confirmed Kevin Warsh as the next Fed Chair on May 13 in the closest vote in the central bank's modern history, and he took over when Jerome Powell's term as chair expired on May 15. Powell is staying on as a governor.

- A blockbuster IPO pipeline came into focus. SpaceX filed its public offering documents on May 20, targeting a roughly $1.75 trillion valuation and a June debut that would rank as the largest IPO in history. The buzz extended across the AI landscape, setting up what could be a landmark stretch for new listings.

- Anthropic, the AI company behind the Claude assistant, confidentially filed for its own IPO on June 1, getting ahead of rival OpenAI; the filing follows a funding round that valued it near $965 billion amid a steep climb in revenue.

- Renewed friction in the Strait of Hormuz late in May and into early June pushed oil and the 10-year Treasury yield modestly higher again, a reminder that the Iran situation remains an unresolved swing factor for energy and rates heading into summer.

Data Dashboard

Stock Market

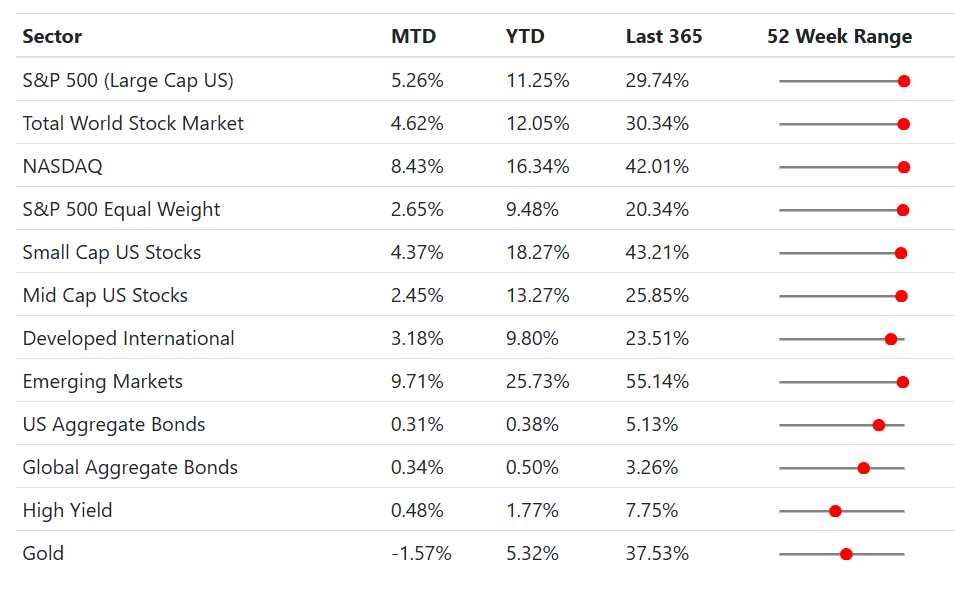

U.S. equities rose for a second straight month, with the S&P 500 gaining 5.26% to finish at a record. Two forces drove the advance: a powerful rebound in megacap technology, and a steady retreat in oil prices that eased the inflation and recession worries hanging over markets since the late-February conflict with Iran. With those pressures lifting and Q1 earnings coming in strong, investors rotated back into the growth names that had been out of favor, lifting the tech-heavy Nasdaq 8.43% on the month.

Sector returns told the rotation story plainly. Technology dominated, far outpacing every other group on renewed AI enthusiasm. A standout feature was the resurgence in software and cybersecurity, corners of tech that had been hit hard earlier in the year on fears that AI agents would erode software business models. As spring earnings showed AI adding revenue rather than cannibalizing it, those names staged a sharp rebound, several posting double-digit single-day gains around their reports. At the other end, Energy fell more than 5% alongside crude, and Utilities dropped about 5% as defensive positioning unwound. The sectors that had cushioned portfolios during the spring's volatility were precisely the ones that lagged.

May sat in the heart of Q1 earnings season, and results gave the rally a firm footing: roughly 84% of S&P 500 companies beat expectations, well above average, with mid-teens earnings growth. The marquee report came from Nvidia on May 20, which posted record quarterly revenue near $82 billion and again raised the bar on AI demand. Notably, the market grew more discerning, rewarding companies that showed clear returns on AI spending and treating those merely raising spending guidance more skeptically. Beneath the surface, breadth narrowed: the cap-weighted S&P 500 (up 5.26%) outpaced its equal-weighted version (up 2.65%), meaning the index leaned once again on its largest names. Internationally, Emerging Markets surged 9.71%, far ahead of developed international (up 3.18%), as the AI trade rippled through heavily weighted Taiwanese and Korean chipmakers.

The IPO market also roared back. SpaceX, now repositioned as an AI infrastructure company after its merger with xAI, filed to go public on May 20 at a valuation near $1.75 trillion, which would rank as the largest IPO ever. It is one of several AI-era names eyeing the market this year, against a backdrop of fierce competition among AI developers. For investors, the theme matters more than any single stock: after a long drought, a wave of large, AI-driven listings is poised to give public markets direct access to companies until now reserved for private investors, along with the heightened scrutiny that public reporting brings.

May Return Summary (by GICS Sector)

Bond Market

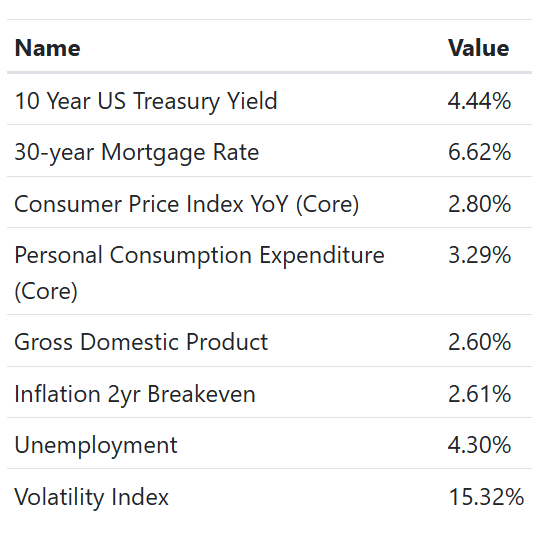

There was no Fed meeting in May, but the central bank still made headlines. The Senate confirmed Kevin Warsh as Chair on May 13 by a 54-45 vote, the narrowest in the modern era, and he took over when Powell's term expired May 15. In an unusual arrangement, Powell remains on the Board of Governors and keeps a policy vote. Warsh has signaled he sees room to lower rates over time while insisting he will set policy independently. With the benchmark held at 3.50%–3.75% in late April, attention now turns to the June 16–17 meeting. The 10-year Treasury yield drifted up to 4.44% from 4.37% a month earlier, as sticky inflation and on-again, off-again Hormuz tensions kept modest upward pressure on rates.

High-grade bond returns were quietly positive, consistent with that small move in yields: the U.S. Aggregate returned 0.31% and the Global Aggregate 0.34%. Bonds continue to offer attractive income by recent standards while providing diversification. Credit reflected the broader risk-on tone, with High Yield up 0.48% and spreads staying contained, a sign investors remain comfortable taking credit risk as the spring's recession fears fade.

Economics

The economy entered mid-2026 on steady footing, with growth running at a 2.6% annualized pace and unemployment holding at 4.3%. That mix of solid-but-not-overheated growth and a historically low jobless rate describes an economy still expanding without obvious strain, with a resilient labor market continuing to support consumer spending.

Inflation remains the sticking point. Core CPI ran at 2.8% year-over-year and Core PCE, the Fed's preferred gauge, at roughly 3.29%, both still above the 2% target. May's drop in oil should relieve some of the headline pressure ahead, and encouragingly, the market's 2-year inflation breakeven eased to about 2.61% from 3.01%, suggesting investors view the energy-driven bump as temporary. On housing, affordability stayed stretched: the average 30-year mortgage rate ticked up to 6.62% from 6.35%, tracking yields higher and keeping a lid on activity.

The dominant global variable remains the Strait of Hormuz. May brought genuine progress toward extending the ceasefire and starting nuclear talks, which drove oil lower, but the situation stayed fluid, with late-month military exchanges briefly reviving supply fears. For now the de-escalation has been a market tailwind; a reversal would quickly feed back into energy prices and rates. Reflecting the calmer mood, the VIX "fear-gauge" eased to 15.32.

Economic Dashboard

Portfolio Changes

In our Global Tactical ETF portfolio, we sold Solar to buy Semiconductors. We also reduced our energy exposure to add diversified commodities.

In our Low Vol Tactical ETF portfolio, we removed foreign fixed income exposure to add in floating rate and senior loan instruments.

Looking into June, three catalysts stand out. First, the Federal Reserve meets June 16–17, the first meeting under Chair Warsh, and markets will parse both the rate decision and the tone of his initial communication closely for any shift in direction. Secondly, the May CPI report lands June 10, the first inflation reading that will show whether the drop in oil prices is beginning to cool headline inflation. The Strait of Hormuz remains a live wire: any movement toward a durable Iran agreement — or away from one will move energy prices and ripple through rates and risk appetite. After two strong months for stocks and a narrowing of market leadership back toward MegaCap tech, this is a good moment to revisit diversification and make sure portfolios aren't overly reliant on a single theme. As always, we're here to talk through any of it with you — please don't hesitate to reach out.

For families with young children, a notable planning item went live on May 28: the Treasury Department launched its "Trump Accounts" app, the main interface for the new tax-deferred savings accounts for children. Children born between January 1, 2025 and December 31, 2028 are eligible for a one-time $1,000 federal contribution, and parents, along with employers, relatives, and others, can add up to $5,000 per year until the child turns 18, with the funds invested for long-term, tax-deferred growth. Account funding and the federal seed deposits begin July 4.

Thanks,

The Friedenthal Financial Team