%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsMarch 2026 - Market Recap

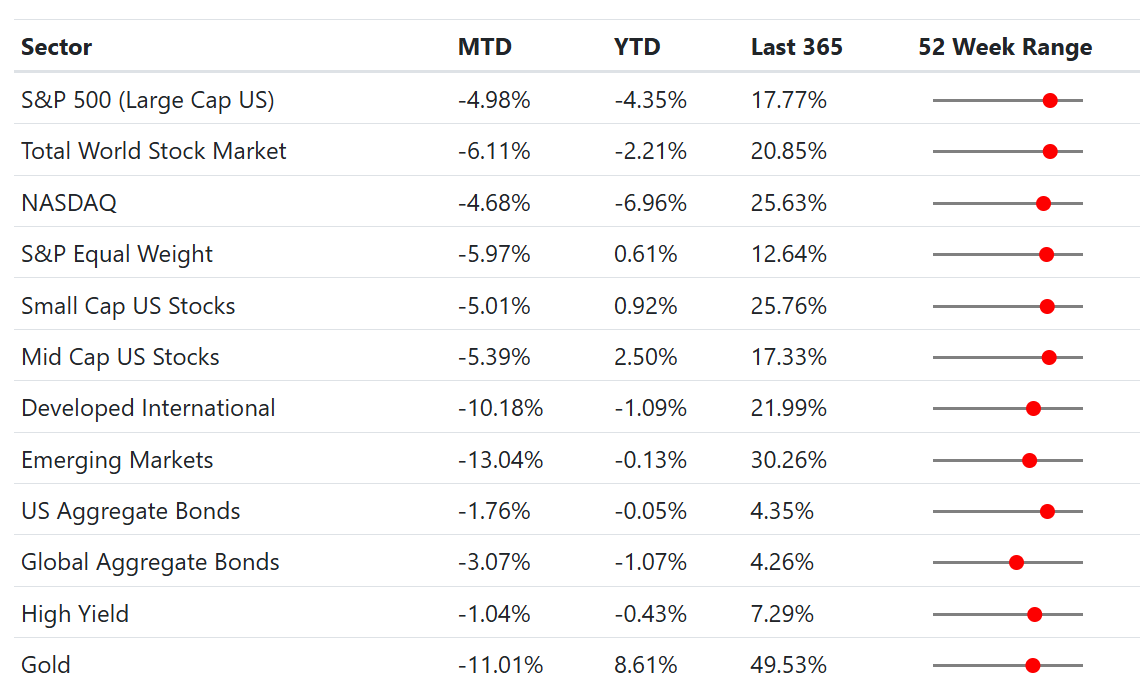

- Global equities sold off sharply in March as the Middle East conflict roiled energy markets and sparked recession fears. Large‑cap U.S. stocks (S&P500) fell nearly 5% for the month, while developed and emerging‑market indexes dropped more than 10% as investors priced in higher geopolitical and inflation risks.

- Oil prices spiked above $100 per barrel. The near‑closure of the Strait of Hormuz, through which roughly 20% of global crude flows, caused tanker traffic to collapse. Energy stocks rallied +10.3% MTD while most other sectors declined, illustrating how a single commodity can drive cross‑asset performance.

- Gold surrendered some of its earlier gains, dropping about 11% MTD, while silver whipsawed - falling from January’s highs to around $72/oz on March 20. Analysts attributed the silver selloff to the Fed’s hawkish hold and a stronger dollar; the decision pushed Treasury yields toward 4.2%, pressuring non‑yielding metals.

Data Dashboard

Stock Market

Equities faced a broad reset in March. The S&P 500 dropped almost 5% as investors digested a confluence of negative catalysts: escalating Middle East tensions, a hawkish Fed on hold, and the prospect of new tariffs and higher inflation. Selling pressure was indiscriminate, with defensive sectors failing to provide the usual shelter. Utilities fell 3.2% and Consumer Staples plunged 8.4%. Growth stocks corrected sharply as Technology declined 4.1%, and Consumer Discretionary lost 6.6%. Within Tech, Software‑as‑a‑Service (SaaS) names were among the hardest hit as investors questioned the durability of their moats in a world where AI agents could commoditize traditional software offerings. The resulting contraction in price‑to‑earnings multiples reflected both a move away from last year’s winners and heightened sensitivity to interest rates.

On the positive side, Energy stocks surged 10.26% thanks to the oil shock; it was the only sector to deliver a gain. With Brent crude averaging $105–115/bbl and WTI $100–110/bbl, energy producers captured substantial free‑cash‑flow tailwinds. Utilities and Financials were the “least bad” decliners (–3.2% and –3.5% MTD), while Industrials (–8.45%), Consumer Staples (–8.41%) and Health Care (–8.11%) were the laggards.

April also marks the start of earnings season, with the large banks typically leading the way. These early reports tend to give a good sense of how the consumer is holding up, and so far, the picture remains fairly steady. There’s a lot of cautious sentiment, but when you look at actual behavior, spending has held up better than expected.

March Return Summary (by GICS Sector)

Bond Market

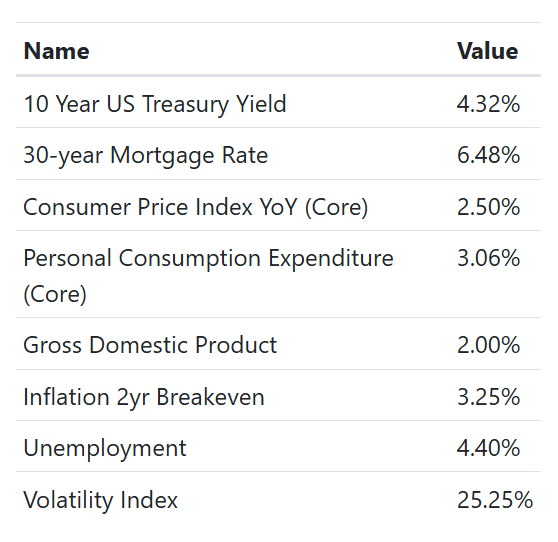

Fixed income offered limited relief. The Federal Reserve left its policy rate unchanged at 3½–3¾% and reiterated that it is “attentive to the risks to both sides” of its dual mandate. With inflation still above target and oil prices surging, markets interpreted the March decision and updated projections as hawkish. The 10‑year Treasury yield drifted higher to ~4.32%, and the yield curve steepened slightly as long‑term inflation expectations moved up (the 2‑year breakeven climbed to 3.24%). U.S. Aggregate Bonds slipped –1.76% on the month, while global bonds fell –3.07% as rising oil pushed interest‑rate expectations higher worldwide. High‑yield spreads widened modestly but remained well below historical stress levels; the sector was down just –1.04%.

The USD gained support from both safe-haven demand and a continued repricing of Fed expectations. As oil moved higher and inflation risks resurfaced, markets pushed back the timing of possible US rate cuts. That helped keep the dollar firm even while most major pairs avoided a full trend breakout.

Economics

The U.S. economy still looks resilient but is showing signs of late‑cycle moderation. Core CPI is running at 2.5% year‑on‑year and Core PCE around 3.06%, indicating inflation remains above target but continues to drift lower. Real GDP growth moderated to 2% annualized, consistent with a slowing but still‑positive trajectory. The unemployment rate held steady at 4.4%, while job creation cooled amid corporate caution and higher borrowing costs. Mortgage rates ticked up again, with the average 30‑year fixed rate climbing to 6.48%, dampening existing‑home sales. Market‑based inflation expectations rose alongside oil prices, pushing the 2‑year breakeven to ~3.24%. Risk sentiment deteriorated, and the VIX jumped to 25.25, reflecting investors’ anxiety about geopolitical escalation and policy uncertainty.

Looking abroad, the IEEPA ruling has immediate global trade implications. By ending the President’s ability to use emergency powers to impose tariffs and invalidating all such duties, the Court forced the administration to rely on narrower trade statutes. The temporary 10% tariff under Section 122 is scheduled to expire in July, leaving companies in limbo about pricing and supply chains. At the same time, rising oil prices are feeding inflation pressures worldwide, and the Strait of Hormuz remains a geopolitical flashpoint. Collectively, these factors point to a more uncertain outlook for growth and prices as we enter the second quarter.

Economic Dashboard

Portfolio Changes

We added more Energy exposure in March, and swapped our Gold Miners position for MSCI Taiwan. We reduced credit exposure in our tactical low volatility portfolio, and are currently overweight on short duration and floating Treasurys. Our sector equal weight approach to the Tactical US stocks portfolio worked well in the March volatilities, with our Energy & Utilities positions outperforming and mitigating losses in other sectors.

April brings a little bit of everything. From taxes, earnings, geopolitics, and questions around the Fed, that can feel like a lot, but the core approach remains the same. Stay disciplined, focus on quality, and keep a long-term perspective. Markets will always give you reasons to react. More often than not, the better approach is to stay steady and let time do the work. As always, we’re here to help guide you through it.

2026 Retirement Contribution Limits

As we step into April, we recommend our clients to be aware of the 2026 retirement contribution limits. If you haven't made a Roth contribution for 2025, the deadline for making one is April 15, 2026.

To keep our clients up to date, we have released an article highlighting the major points.

Please feel free to reach out with any questions about IRA distributions (including RMDs), taxes, 2026 contributions or just markets in general.

Thanks,

The Friedenthal Financial Team