%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsJuly 2025 - Market Update

- The S&P 500 closed July at a fresh record high, driven by mega-caps buoyed by upbeat earnings and renewed AI capex commitments.

- At its July 30–31 FOMC meeting, the Fed held the federal funds rate steady, citing tariff uncertainty and a robust labor market.

- On July 31, President Trump issued an executive order imposing new reciprocal tariffs effective August 8 on countries without a trade agreement.

- The U.S. dollar rebounded 1.9% in July, while the Bloomberg U.S. Aggregate Bond Index posted a modest monthly decline.

- During Crypto Week (July 14–18), the GENIUS Act passed the House July 17 and was signed July 18, the CLARITY Act cleared July 18, and Texas enacted the nation’s first state-managed Bitcoin reserve.

Data Dashboard

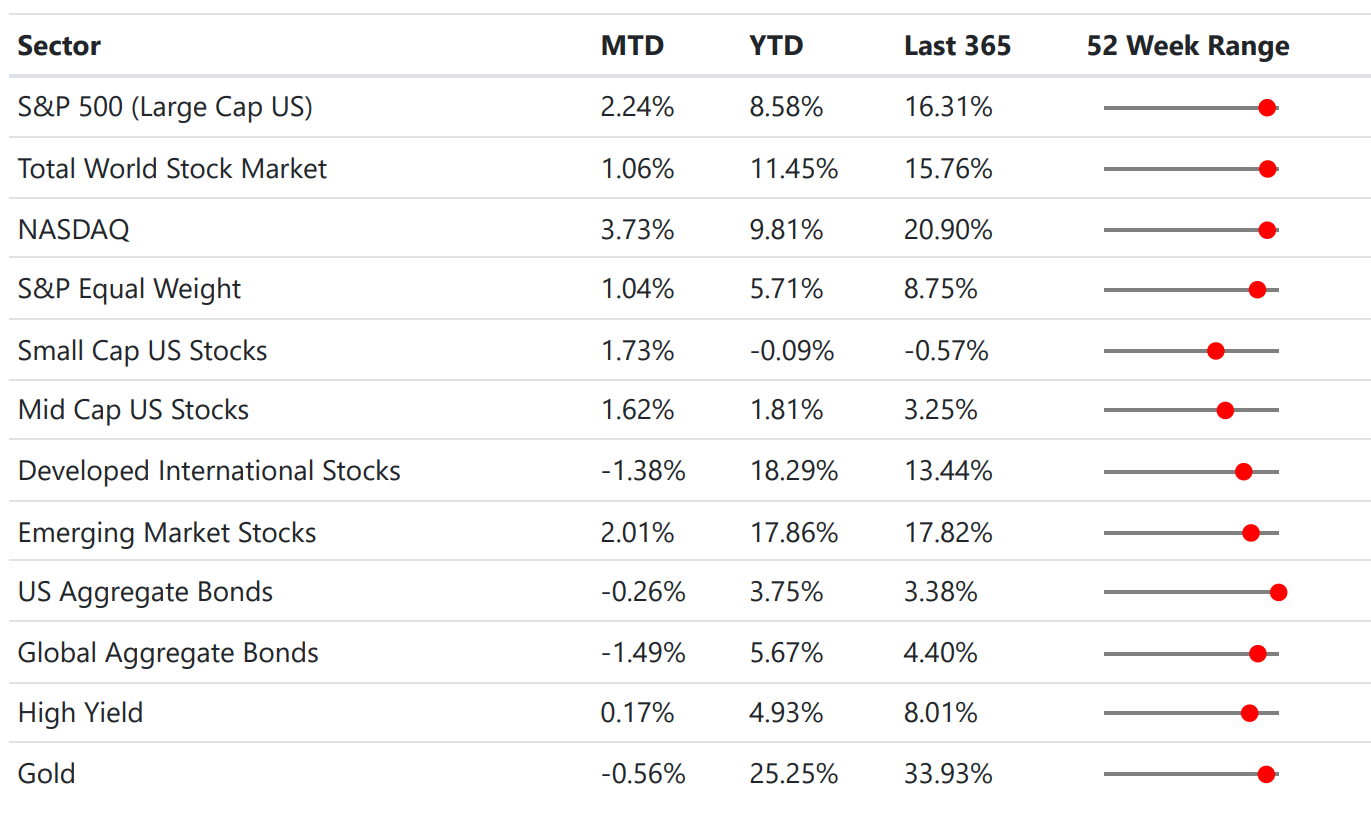

Stock Market

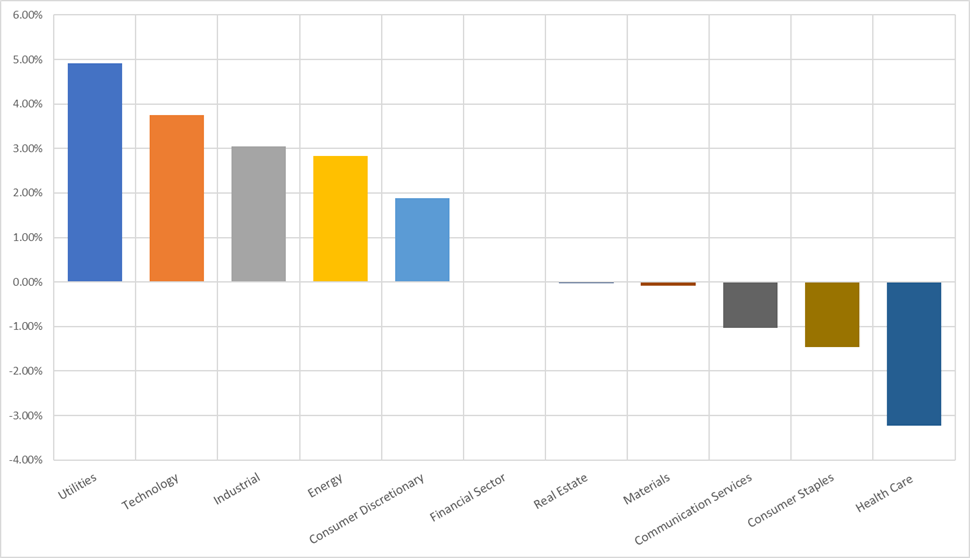

Tech stocks posted solid gains in July driven by positive trade policy developments, better than expected corporate earnings & a strong labor market. Most hyperscalers reiterated their commitment to capex spending on AI. Utilities and Technology were the best performing sectors for the month, while Healthcare was the worst, extending their underperforming streak. Nvidia ended the month as the most valuable company in the world, with a market capitalization of US$ 4.36 Trillion.

Trade agreements were a key driver of market performance, as the U.S. secured multiple deals—including with the EU and Japan—ahead of the August 1 deadline. Meanwhile, negotiations with China advanced, prompting Treasury Secretary Bessent to express optimism, even as tensions with Canada persisted and a federal appeals court considered the legality of existing tariffs. Investors appeared more encouraged by the reduced policy uncertainty than by any particular tariff levels, and momentum in AI helped offset tariff-related headwinds in certain sectors.

Meanwhile, roughly two-thirds of S&P 500 companies have reported Q2 2025 results, with nearly 80% beating EPS estimates. On both a year-to-date and trailing-365-day basis, large-cap market-cap indices have outperformed their equal-weight counterparts as well as small- and mid-cap stocks.

July Monthly Returns (by Sector)

Bond Market

Treasury yields climbed alongside rising inflation expectations, even as the Federal Reserve held short-term borrowing rates steady. Longer-term rates outpaced their short-term counterparts amid mounting worries over the U.S. budget deficit and a more prolonged pause in rate cuts than initially anticipated.

High-yield corporate bonds delivered positive returns for the month, owing to their lower sensitivity to long-term rate movements. Since early April, the 10-year Treasury yield has remained in the 4.0-4.5% range, as investors await greater clarity on trade policy, Federal Reserve actions, and the broader direction of the U.S. economy.

Economics

Economic indicators for the month presented a mixed picture. June payrolls surpassed forecasts and the unemployment rate dipped to 4.1%, though job growth is anticipated to decelerate in July. Initial jobless claims declined for six straight weeks before edging up, while continuing claims remained elevated.

Both CPI and PPI readings came in cooler than expected, yet housing data was broadly weak and the average 30-year fixed mortgage rate held nearly flat in July—underscoring ongoing low activity in the housing market.

At its July meeting, the Federal Reserve delivered hawkish signals with no hint of a September rate cut, and tensions between President Trump and Fed Chair Powell added to market uncertainty. Looking ahead, August will wrap up Q2 2025 earnings season and deliver fresh data on employment, inflation, and GDP; although the Fed does not reconvene until mid-September, August’s releases are likely to be pivotal for its next policy moves.

July Economic Dashboard

.png)

Portfolio Changes

Over the years, American stocks have outperformed their global peers—a trend driven in part by sector weights, stronger economic conditions than those in other developed countries, and a robust U.S. dollar. In our view, U.S. investors earn little compensation for bearing foreign-currency risk, and the added diversification benefits have been minimal.

However, in 2025 the dollar weakened amid concerns about the Federal Reserve’s independence, renewed tariff uncertainty, and a broader shift away from the U.S. dollar. Accordingly, in many of our strategic portfolios, we replaced Developed International (EFAV) and Emerging Markets (EEMV) allocations with their currency-hedged counterparts.

In our tactical ETF portfolio, we added exposure to Metals & Mining, Semiconductors, and South Korea, while trimming Europe and Communication Services. We’ve maintained our Gold Miners position, which has performed strongly in today’s volatile macroeconomic environment.

In our tactical low-volatility portfolio, we reduced credit exposure in favor of short-duration and floating-rate instruments. With the Fed signaling “higher for longer,” those shorter-duration yields continue to look attractive.

General Client Considerations

The IRS increased the 2025 annual contribution limits for 401(k), 403(b), most 457 plans, and Thrift Savings Plans (TSP) from $23,000 to $23,500. Even in the second half of the year, adjusting your contribution elections can help you spread contributions more evenly over the remainder of the year and maximize your tax-advantaged retirement savings. If you're participating in a company-sponsored retirement plan and plan to max out your contributions, be sure to check with your HR department to confirm your contribution amount reflects the new limits.

Additionally, if you are 50 or older, the catchup contribution limit for 401(k), 403(b) and TSPs has remained the same at $7,500. If you are born in 1975 or earlier, you can contribute up to $31,000 to these accounts in 2025. You do not have to wait until your 50th birthday to make catchup contributions - the contributions can start on January 1st of the year you turn 50.

Starting 2025, if you are aged between 60-63, you can contribute up to a total of $34,750 (eligible for a higher catch-up contribution due to SECURE 2.0).

For more information, check out our newsletter on 2025 Retirement Account Limits.

As always, reach out with any questions or concerns.

Thanks,

The Friedenthal Financial Team