%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsJanuary 2026 - Market Recap

- The Fed held interest rates steady at their Jan FOMC meeting. The President tapped Kevin Warsh as the next Federal Reserve Chair.

- Energy (+14%) and Materials (+8.6%) surged on rebounding commodity prices, while Technology (flat) and Financials (–2.4%) lagged after 2025’s big gains. Broad market leadership improved, lifting small-cap stocks (+5.4%) more than tech-heavy Nasdaq (+1.0%)

- Gold jumped +12% in January as investors sought inflation hedges, and silver skyrocketed nearly +63% before a speculative frenzy collapsed in a single –26.5% plunge (its worst one-day loss since 1980). This wild swing in silver’s price reflected heightened speculation and a swift shift in investor sentiment.

- International equities continued to outperform US equities, while the US dollar declined 1.35% for the month.

Data Dashboard

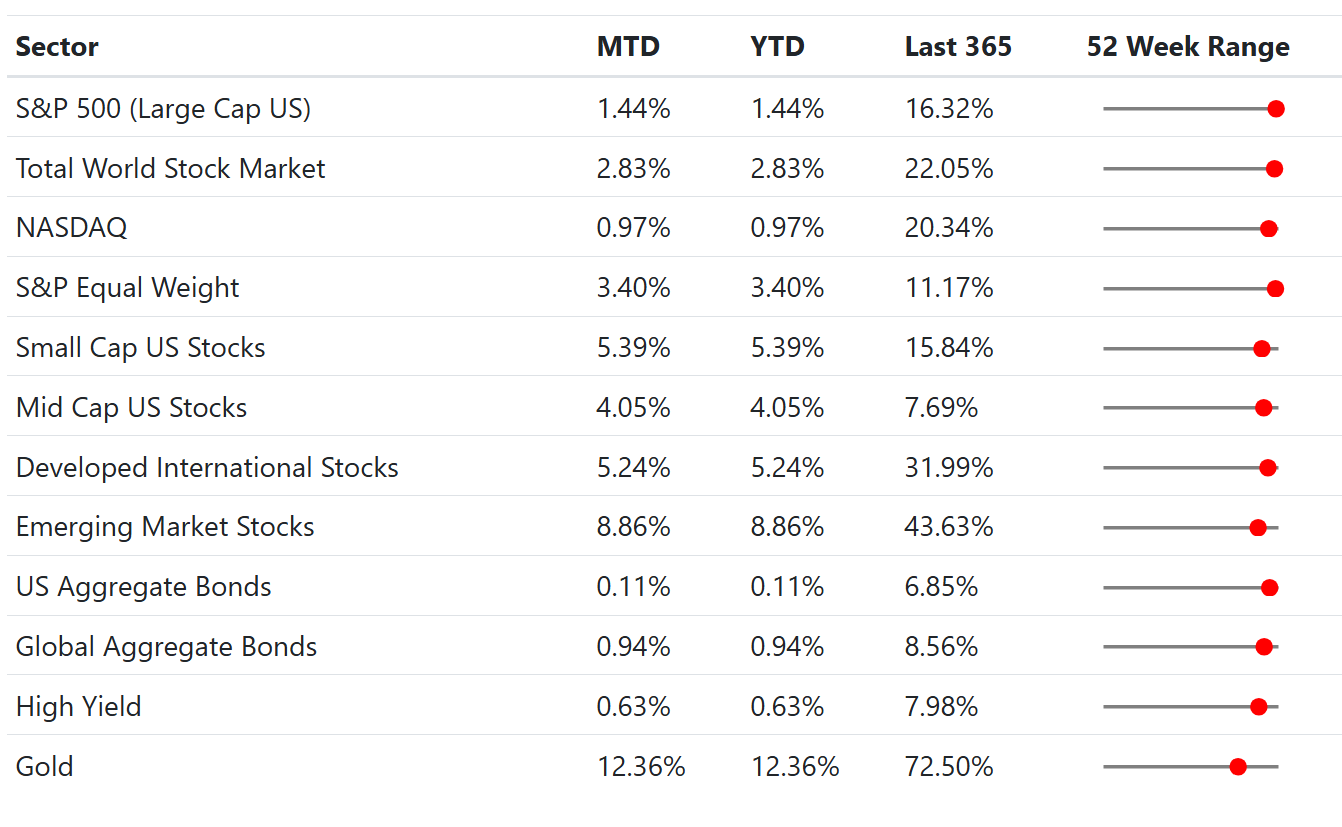

Stock Market

The S&P 500 notched a 1.4% gain for January, a decent start following last year’s big rally. Notably, global equities outperformed the U.S. – the MSCI Developed International index rose 5.2%, and Emerging Markets surged 8.9%. Investors poured into overseas markets amid improving economic outlooks abroad and a slightly weaker US dollar, lifting foreign equities more than domestic indices. Within the US, market leadership broadened beyond 2025’s mega-cap tech winners. Smaller companies and value/cyclical stocks took the lead, a healthy sign that the rally is widening to more areas of the market.

A major theme was sector rotation. The tech-heavy Nasdaq was up just 1% and previously underperforming sectors like energy, industrials, materials, and consumer staples powered ahead, posting mid- to high-single-digit gains. This rotation reflected investors shifting toward stocks tied to economic recovery and inflation beneficiaries, while taking profits in stretched growth/tech names. Positive economic signals, such as stable growth and easing inflation, encouraged a tilt toward cyclicals and international markets where valuations looked more attractive.

Energy was the best performing sector, skyrocketing 14.2% for the month, as oil prices rebounded from last year’s lows, buoyed by renewed demand optimism and supply constraints. Materials also rose 8.6%, helped by rising industrial metal prices and hopes for increased global infrastructure spending. Consumer Staples (+7.5%) and Industrials (+6.7%) posted healthy gains as well, indicating investors’ growing preference for economically sensitive or defensive value stocks over high-growth plays.

Technology and Health Care were flat in January, and the only losing sector in January was Financials, which declined –2.4%. Bank and insurance stocks struggled amid string earnings reports, but concerns about the private credit space & medicare increase caps. Overall, the shift in sector leadership toward energy, materials, and other cyclicals suggests the market is pricing in a brighter economic outlook and possibly higher inflation or commodity demand – trends we are monitoring closely.

Investor sentiment remained broadly optimistic, but pockets of froth emerged. This was nowhere more evident than in precious metals, particularly silver. Early in the month, a speculative fervor gripped the silver market, sending prices up ~63% in an astonishing short-term surge. Enthusiastic retail traders and momentum-driven funds piled in, fueled by inflation hedging themes and perhaps FOMO (fear of missing out). However, that euphoria proved fleeting: silver prices suddenly reversed course in late January, plunging about 35% intraday after Kevin Warsh was announced as the President's nominee for Fed chair. This was silver's largest single-day collapse since 1980’s infamous crash. This dramatic round-trip for silver serves as a reminder that rapid, sentiment-driven spikes often end just as sharply. Gold, while also rising sharply, saw a less dramatic pullback, as investors continued to seek safety and inflation protection.

January Return Summary (by GICS Sector)

Bond Market

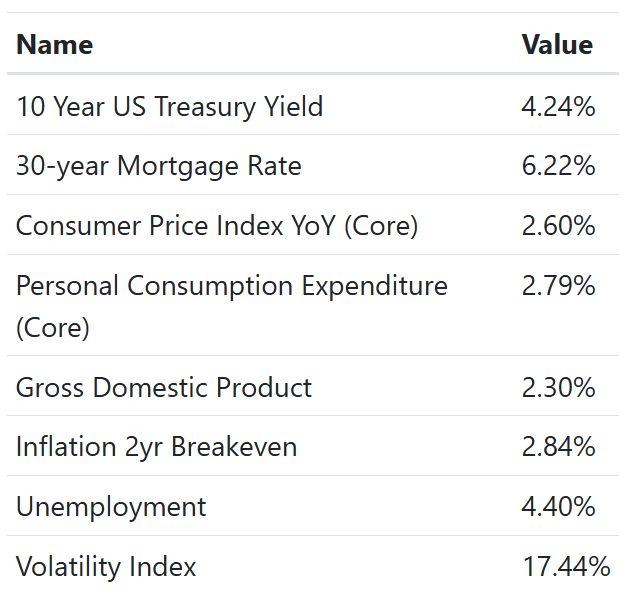

The bond market remained stable in January, with the 10-year U.S. Treasury yield staying relatively range-bound and ending the month at 4.24%. The Federal Reserve’s decision to hold the federal funds rate steady at 3.50%–3.75% restricted further yield increases.

The shift in sentiment contributed to a modest steepening of the yield curve; short-term rates remained anchored by the Fed’s pause, while longer-dated yields ticked upward as investors braced for a more hawkish long-term policy stance.

Investment-grade bonds were largely flat, with the Bloomberg US Aggregate Bond Index returning a modest 0.11%. Global bonds outperformed their U.S. counterparts as the Global Aggregate Bond Index rose nearly 0.9%, bolstered by a generally softer U.S. dollar and cooling inflation in the Eurozone. U.S. high-yield bonds climbed 0.6%, supported by a "risk-on" sentiment in equity markets and stable corporate default outlooks. Investors remain in a holding pattern, collecting coupon income while awaiting definitive signals on when the Fed will pivot to further cuts, a prospect currently anchored by persistent inflation and the upcoming leadership transition.

In January 2026, the private credit market demonstrated resilience despite a challenging year-end in 2025 marked by high-profile bankruptcies and rising scrutiny of borrower liquidity. Leading into this year, the market witnessed a steady expansion toward a $2 trillion asset class, even as default rates reached as high as 5.7% in late 2025. A defining trend of the recent months has been the surge in "selective defaults," where lenders utilize payment-in-kind (PIK) structures to assist borrowers struggling with high interest coverage. By early 2026, the percentage of new loans issued with PIK flexibility climbed to 22.2%, reflecting both competitive structuring and a strategic pivot toward preserving borrower liquidity in a "higher-for-longer" rate environment.

Economics

The macroeconomic backdrop entering 2026 is one of cooling inflation and steady, moderate growth. The US GDP expanded 4.4% in Q3 2025, with the YOY GDP growth at 2.30%, indicating the economy expanded at a healthy but not overheated pace in late 2025. The Consumer Price Index (CPI excluding food and energy) is rising 2.6% year-over-year on a core basis, and the Fed’s preferred Core PCE index is up about 2.8% YoY. Both measures are down significantly from peaks and are edging closer to the Fed’s 2% target, though not quite there yet. Importantly, longer-term inflation expectations (2-year TIPS breakeven rate ~2.8%) are well-contained.

The labor market remains relatively strong, but with some signs of cooling. The unemployment rate ticked up to 4.4% from around the low-4% range. However, 4.4% unemployment is still historically low and points to a generally robust job market supporting consumer spending. Wage gains have tempered but are still positive, helping consumers navigate the higher cost of living even as inflation slows. However, the Federal Reserve cautions that they're watching the labor market closely, as the focus is shifting away from inflation.

Meanwhile, other economic indicators provided mixed but generally encouraging signals. Mortgage rates have eased to around 6.2% for a 30-year loan, down from last year’s highs above 7%. This has begun to breathe a bit of life back into the housing market. We’ve seen upticks in homebuyer interest and refinancing activity as borrowing costs come down. The Volatility Index (VIX) rose only modestly to the mid-17 range in January despite the stock market rotation and the silver drama; overall financial conditions remain benign. Consumer and business confidence indicators are fairly upbeat to start the year, reflecting optimism that the economic expansion can continue in 2026. We will be watching February’s data on inflation and jobs closely for any inflection points, but so far the economy appears to be navigating the desired soft landing path.

Economic Dashboard

Portfolio Changes

Our tactical portfolios benefitted from our sector equal weighted approach in the broadening market environment of January. We held on to our allocations in Gold miners in our tactical ETF portfolio. We also swapped out our clean energy, oil services & semiconductors, for Japan, Uranium and Healthcare. We also reduced credit in our low-vol tactical portfolio, for mortgage-backed and short duration instruments.

Thanks,

The Friedenthal Financial Team