References

- “Harvest Portfolios" Currency Hedged vs Unhedged ETFs

%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsIn a global market, diversification is essential — but so is understanding what you’re really exposed to when you invest internationally. Many U.S.-based investors wisely allocate part of their portfolios to foreign equities for broader growth opportunities and diversification benefits. However, they often overlook a hidden layer of risk: foreign currency exposure.

This blog explains why we favor currency-hedged foreign equity ETFs — like HEFA (iShares Currency Hedged MSCI EAFE) and HEEM (iShares Currency Hedged MSCI Emerging Markets) — over their unhedged counterparts, EFA and EEM, for our U.S.-based clients.

When you buy international stocks, you’re buying two sources of returns (and risk):

In theory, this currency exposure can add diversification. In practice, it often doesn’t compensate investors for the extra volatility. Research has shown that currency fluctuations are random over the short term and can offset or amplify local equity returns in unpredictable ways.

The chart below shows the difference in performance between the currency hedged & unhedged ETFs of the MSCI EAFE index, over the last 10 years.

The U.S. dollar has a strong long-term track record. Since the 1980s, it has appreciated against many major currencies due to the U.S. economy’s scale, its central role in global trade, and its reserve currency status. While the dollar experiences cycles — sometimes strengthening, sometimes weakening — there’s no guarantee that currency swings benefit long-term equity investors.

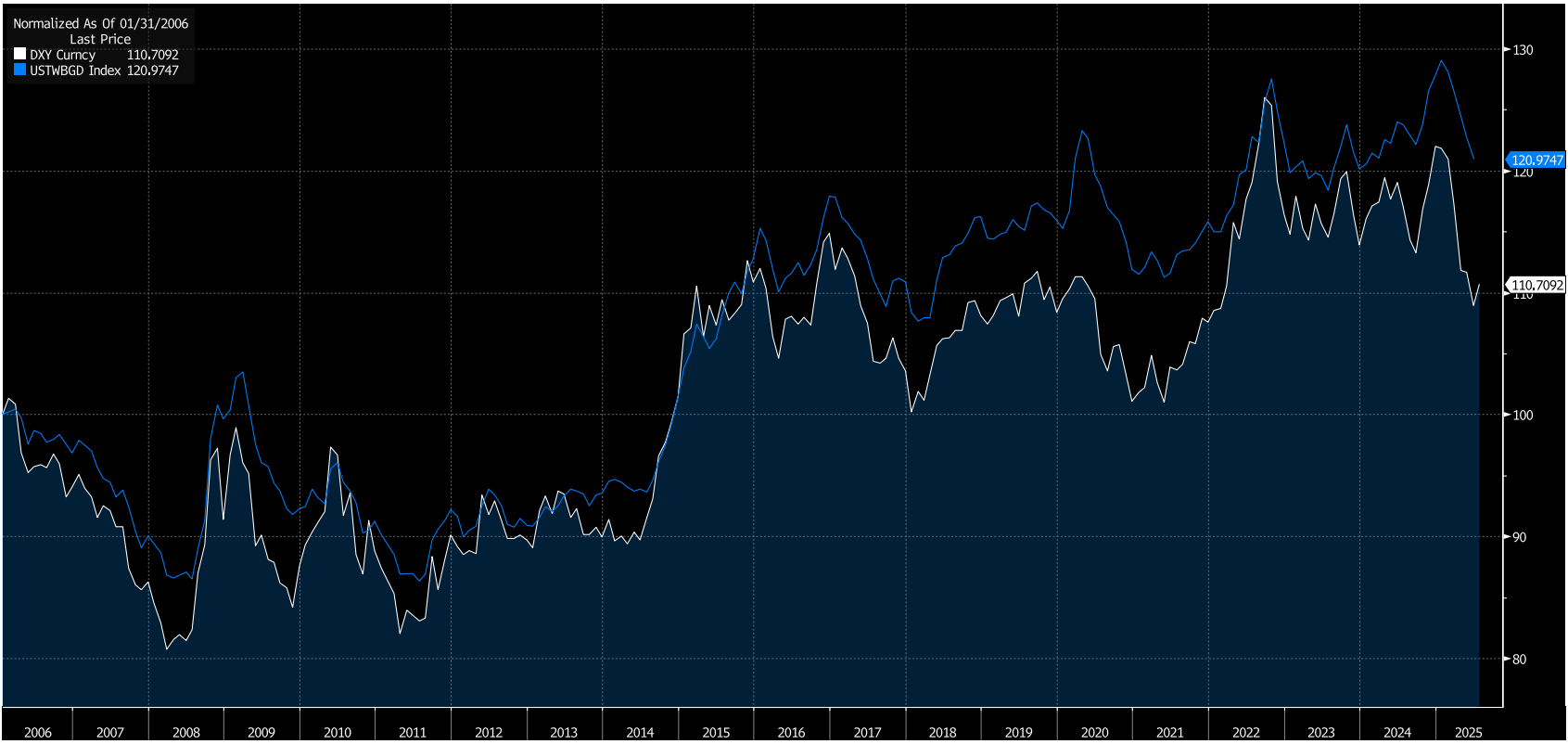

A simple measure of broad dollar strength is the U.S. Dollar Index (DXY) — the most widely watched index for tracking the value of the U.S. dollar. It measures the dollar’s value against a basket of six major developed market currencies: the euro, yen, pound, Canadian dollar, Swedish krona, and Swiss franc.

While the DXY is useful, it doesn’t include emerging market currencies, which make up a large portion of broad international equity exposure. For a more comprehensive picture, many economists and policymakers also monitor the Federal Reserve’s Broad Trade Weighted Dollar Index, which covers both developed and emerging market currencies, and is rebalanced annually to reflect changing trade flows. This broader measure is often more relevant for understanding how the dollar is performing against the currencies of America’s global trading partners.

The first half of 2025 is a timely reminder of why this matters. The dollar weakened significantly — the DXY Index dropped about 12% as markets responded to rising fiscal concerns, shifting monetary policy expectations, and trade tensions. Investors who held unhedged foreign equity positions benefitted from this drop because foreign currencies strengthened against the dollar, boosting their returns in USD terms.

However, such periods can be fleeting. Over multiple cycles, the dollar’s strength often reasserts itself, and investors who hedge currency risk avoid having their equity gains offset when the dollar regains ground.

It’s important to acknowledge: currency hedging will underperform when the dollar weakens. There will always be periods — like early 2025 — when unhedged investors benefit from a falling dollar. This is the trade-off: giving up occasional upside in exchange for more consistent, predictable exposure that matches clients’ real-world liabilities (which are in USD).

We believe that for most U.S.-based clients, foreign currency exposure is an uncompensated risk. Hedging helps keep your international allocation focused on what matters — the performance of the companies you own — while reducing surprises that come purely from exchange rate swings.

While there will be periods when a weakening dollar means hedged positions underperform, the long-term goal is a more stable, predictable return stream that aligns with your U.S.-based spending needs.

Its important to note that currency hedging isn’t free—ETFs pay to roll FX forwards, and the net “carry” depends on interest-rate differentials (it can help when U.S. rates are higher, and hurt when they’re lower). Hedged ETFs also tend to have higher expense ratios and a bit more tracking error than unhedged versions, so compare after-fee results when deciding your hedge.

Currency movements are unpredictable, and for most investors, they don’t offer meaningful return benefits over the long term. Staying hedged helps you capture international equity growth without the unnecessary risk of currency noise.

If you’d like to talk more about how to position your portfolio — or explore whether hedged or unhedged exposure makes sense for your goals — let’s have that conversation.