%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsFebruary 2026 - Market Recap

- Geopolitical tensions flared as the US conducted airstrikes against Iran on Feb 28, pushing oil prices sharply higher and reigniting market volatility early March.

- Defensive sectors outperformed in February. Utilities, Energy and Materials were the best performing sectors, while Tech and Financials were the worst performers.

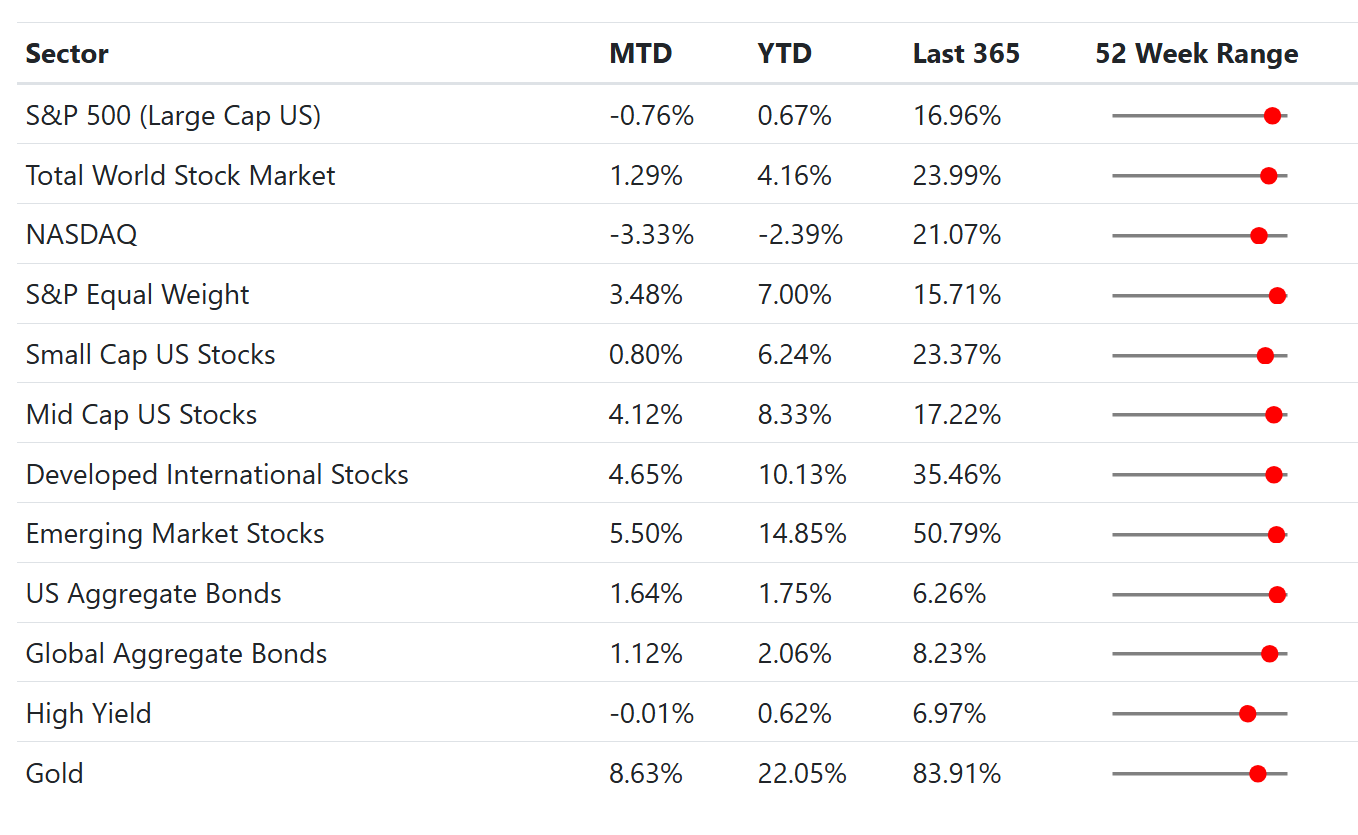

- Gold continued its bull run through February, returning 8.63% for the month

- The Supreme Court issued a landmark ruling on Feb 20, striking down the sweeping tariffs imposed by President Donald Trump in a series of executive orders.

Data Dashboard

Stock Market

February’s market looked mixed on the surface, but it was highly active underneath. Large‑cap benchmarks were held back by weakness in a narrow slice of mega‑cap growth and AI‑adjacent software, while equal‑weight and mid‑cap/value exposures posted their strongest relative results in months. Many investors experienced a “two markets” dynamic: the well‑known index leaders cooled, while a broad set of sectors quietly strengthened. The S&P 500 Equal Weight Index surged 3.5%. Small- and mid-caps also outperformed (2.7%), suggesting that market participation is broadening as investors look beyond the narrow leadership of the "Magnificent Seven."

Utilities was the best performing sector in February while Tech & Financials were the worst performing, as investors reassessed valuations amid shifting trade policies and jittery risk appetite. Within the Tech sector, a particularly hard-hit segment is the SAAS/Software space, which has experienced significant PE contraction (reduction in lofty Price-to-Earnings multiples). This 'de-rating' reflects a market increasingly skeptical of traditional software moats in the face of rapid AI agent adoption; investors are now pricing in the risk that autonomous agents could disrupt the established workflows and pricing power that once defined these industry leaders.

By late February, the market focus shifted to the Middle East as the U.S. launched Operation Epic Fury following regional escalations. The action on February 28 sent oil prices higher, contributing to Energy’s strong monthly performance and lifting defense stocks. While equity markets showed initial jitters, they showed resilience into the close, suggesting investors are weighing the immediate commodity spike against a broader economic backdrop that remains stable.

February Return Summary (by GICS Sector)

Bond Market

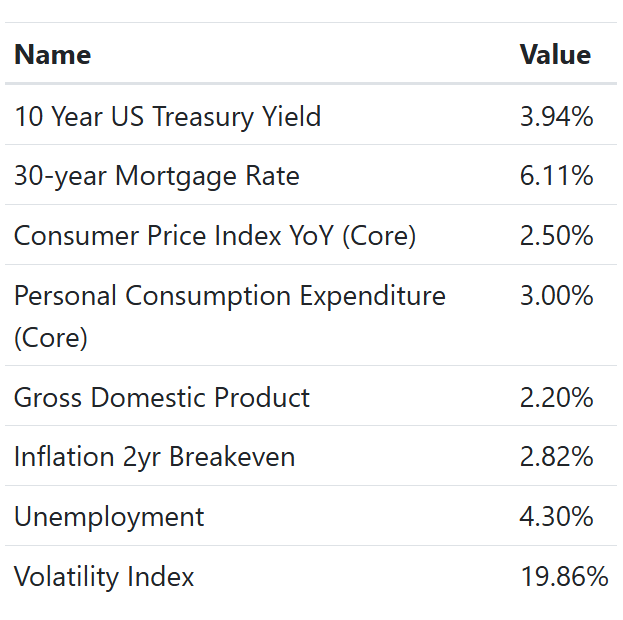

Fixed income markets were generally positive in February. The 10-year Treasury yield drifted lower to 3.94%, reflecting a flight to quality as geopolitical risks rose and a recalibration of inflation expectations. Consequently, the U.S. Aggregate Bond Index rose 1.64%, while global bonds lagged slightly at 1.12%, while the US dollar index rose slightly. High yield bonds however, remained almost flat as the credit spreads increased from ~2.65% to 2.95% in February.

For the first time since Sep'22, the average 30Y fixed mortgage rate fell to 6.12% in the final week of February. This dip in rates ignited a mini rush to refinancing. Affordability remains a challenge with higher home prices. New listings remain somewhat constrained, falling 3% from Feb'25. However, total active inventory is up 5% compared to last year.

Economics

The economy remained on solid footing in February, with GDP growth estimated at 2.2%, supported by strong labor force participation and stable consumer activity. Inflation continues its gradual cooling trend: Core CPI printed at 2.5% YoY and Core PCE hovered near 3.0%. Encouragingly, market-based inflation expectations held below 3%, providing the Fed with potential flexibility as it weighs the timing of rate cuts later this year. The swaps markets are currently pricing in less than two 25bp rate cuts in 2026.

Unemployment remained steady at 4.3%, while the Volatility Index (VIX) ticked up to 19.86 amid late-month geopolitical concerns. Importantly, mortgage rates edged down to an average of 6.11%, helping housing activity stabilize after a soft end to 2025.

The most significant policy shift of the month occurred in the legal arena. On February 20, the Supreme Court struck down broad executive tariff powers in Learning Resources, Inc. v. Trump. The Court ruled that the President cannot use the International Emergency Economic Powers Act (IEEPA) to impose revenue-raising tariffs without explicit Congressional authorization. This led to the termination of several existing trade levies on February 24. While the ruling eased immediate inflationary pressure on imported goods, it has introduced new questions regarding federal revenue and future trade negotiations.

Economic Dashboard

Portfolio Changes

In our tactical ETF portfolio, we added Latin America. We have also replaced our Uranium ETF for VanEck Oil Services. Our metals allocations remains consistent, as we replaced lithium for copper.

In our tactical low vol portfolio, we continue to prefer more credit risk and lower duration risk, with periodic exposure to convertibles and high yield securities.

2026 Retirement Contribution Limits

As we step into March, we recommend our clients to be aware of the 2026 retirement contribution limits. Additionally keep in mind, if you haven't made a Roth contribution for 2025, the deadline for making one is April 15, 2026.

To keep our clients up to date, we have released an article highlighting the major points.

Please feel free to reach out with any questions about IRA distributions (including RMDs), taxes, 2026 contributions or just markets in general.

Thanks,

The Friedenthal Financial Team