%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsDecember 2025 - Market Recap

- The Federal Reserve lowered the FOMC rate by 25bps at its December meeting. The decision reflects a split between supporting the labor market and concerns about inflation, with more focus on the former.

- Rate-sensitive sectors lagged – Utilities sank 5.1% and Real Estate fell 2.1% in December amid pressure from elevated yields.

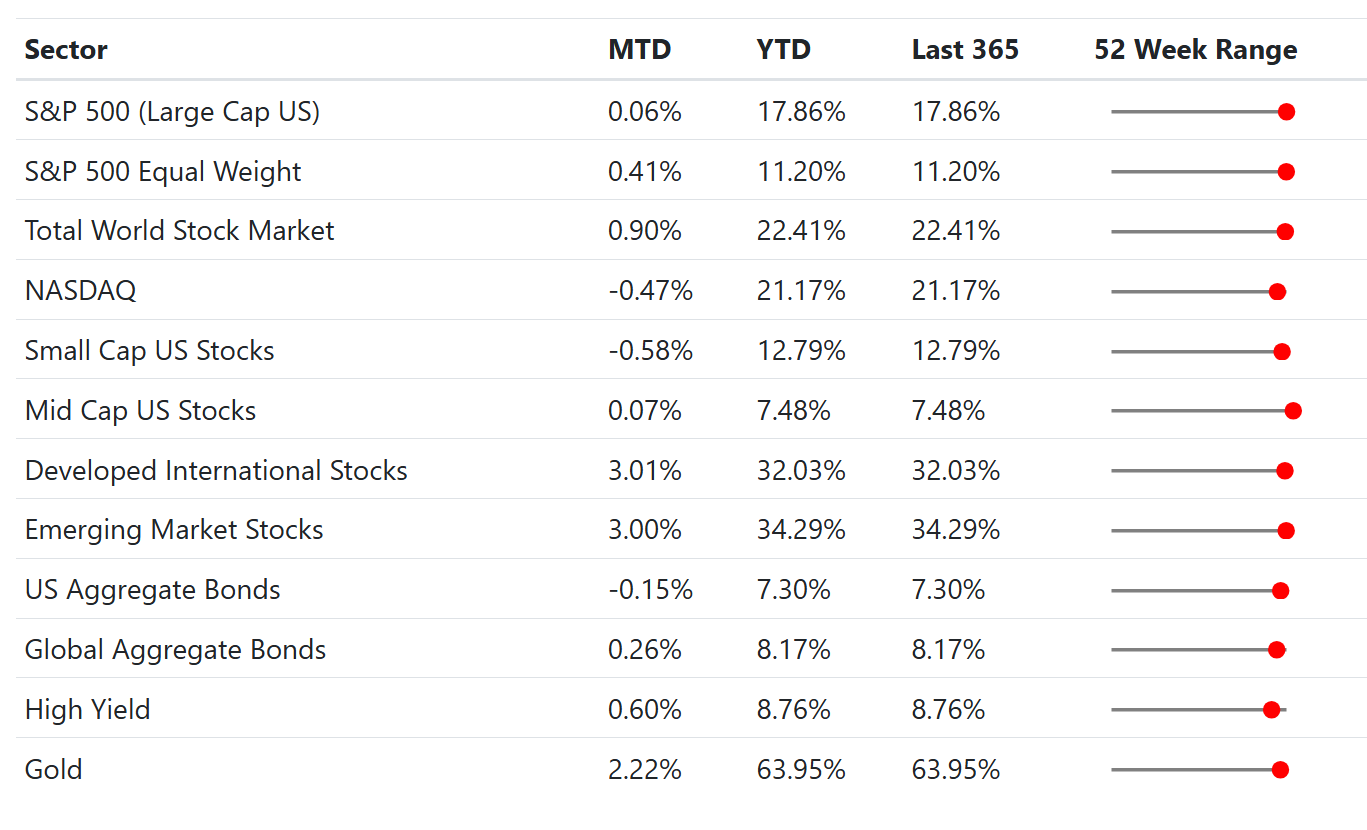

- Major equity indexes were mixed: the S&P 500 was essentially flat for the month, while international stocks posted gains north of 3% in December alone.

- Both Emerging Markets and Developed International stocks returned >30% in 2025, outperforming US markets (both market-cap weighted and equal-weighted), further benefitting from the decline in the US dollar.

- Consumers remained resilient during the holidays. US retail sales rose roughly 4% YoY, as shoppers hunted for deals amid tighter budgets.

- Gold extended its rally, gaining about 2.2% in December and nearly 64% for the full year, reflecting strong safe-haven and diversification demand. Silver had an absolutely terrific year, up 148% in 2025.

Data Dashboard

Stock Market

Equity markets closed out 2025 with a whimper rather than a bang. December trading was characterized by year-end positioning and sector rotation. Mega-cap technology stocks paused after their strong run. The tech-heavy Nasdaq Composite dipped about −0.5% for the month, while value and cyclicals took the lead. Financials rallied +3.1% to top the sector rankings, aided by stable credit conditions and a steepening yield curve. Materials and Communication Services also notched solid gains, each up around +2%. In contrast, high-duration, rate-sensitive groups struggled: Real Estate and Utilities were the worst performers, down −2.1% and −5.1% respectively. This rotation underscores how elevated interest rates may continue to shape sector leadership, with investors favoring areas less vulnerable to borrowing costs.

Despite the intra-market churn, broad indexes showed little movement in December. The S&P 500 ended essentially flat, hovering near record levels and preserving its robust +17.9% yearly gain. Smaller stocks underperformed slightly – the Russell 2000 fell −0.6%, suggesting some late-cycle caution around economically sensitive companies. Notably, international equities outpaced U.S. markets for the month. Developed market stocks rose around +3%, and emerging markets added roughly +3%. After months of U.S. mega-cap dominance, 2025’s finale saw a broader global balance. Emerging market equities finished the year up over +34%, marking their best annual performance since 2017. Going into 2026, we believe maintaining diversification across regions and sectors remains prudent, as market leadership can shift quickly in a maturing bull market.

December Return Summary (by GICS Sector)

Bond Market

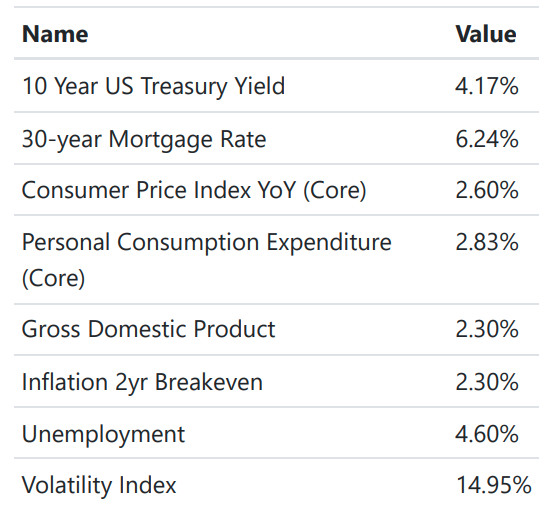

The bond market took a breather in December. Treasury yields held relatively steady. The benchmark 10-year U.S. Treasury yield hovered around 4.17% at year-end, a touch lower than its peak earlier in 2025. This stability kept bond price moves modest. The U.S. Aggregate Bond Index posted a slight −0.15% return for December, essentially flat, and finished the year up about +7.3% – a welcome positive year after 2022’s losses. Global bonds managed a small gain of +0.26% on the month, aided by declining yields in some overseas markets and a mild U.S. dollar pullback.

Crucially, credit conditions remained benign. Corporate bond spreads (the extra yield over Treasuries) stayed historically tight, indicating that investors are still comfortable taking credit risk. High-yield bonds in particular held their value. The flagship high-yield index rose about +0.6% in December and defaults remain low. Yields across the bond spectrum continue to offer attractive income by recent standards. We believe this income profile may provide a cushion for balanced portfolios. Looking ahead, if inflation keeps softening, the Fed’s next move could be a rate cut later in 2026, an environment in which bonds can perform well. Even in a steady-rate scenario, today’s higher starting yields mean bonds may contribute both income and diversification benefits after several years of playing second fiddle to stocks.

Economics

The late-2025 economic picture shows encouraging progress on inflation with hints of late-cycle dynamics. Price pressures have cooled markedly: Core CPI is running at 2.6% year-over-year and core PCE around 2.8%, the closest inflation has been to the Fed’s 2% target in over two years. This progress, aided by improved jobs data, prompted the Fed to cut the federal funds rate by 25 basis points at its December 10 meeting to a range of 3.5%–3.75%. Consumers are benefiting from the easing of price growth, as real wages have begun rising again in many sectors. Initial jobless claims came in at 191,000, lower than expected, although the unemployment benefit filings are sometimes distorted by the Thanksgiving holiday.

While the labor market remains structurally sound, there are clear signs of a transition toward a late-cycle environment. The unemployment rate reached 4.6% in late 2025, its highest level since late 2021. Despite some high-profile layoffs, the market remains tight; initial jobless claims hit a three-year low of 191,000 over the Thanksgiving period, though filings rose to 199,000 toward the end of December. Contrary to expectations of a slowdown, the U.S. economy actually accelerated in the second half of the year, with Q3 GDP growing at a robust 4.3% pace. Consumer spending has remained the primary engine of this growth, with resilient holiday retail sales—bolstered by heavy discounting and a "buy now, pay later" surge—supporting the economy despite years of high borrowing costs.

One area feeling the pinch of past rate hikes is housing. Housing affordability remains stretched, but there are signs of relief at the margins. The average 30-year mortgage rate is about 6.24%, down from its peak above 7% in 2024. Home price appreciation has decelerated significantly, and some overheated markets have seen prices flatten or dip, which may eventually entice buyers back. Still, high financing costs and limited supply are keeping a lid on housing activity. In broader terms, the economy appears to be moving into a slower-growth, lower-inflation phase – exactly what the Fed has been aiming for. We’ll be watching metrics like wage growth, consumer confidence, and manufacturing trends for any early warning signs as the cycle matures.

Economic Dashboard

Portfolio Changes

In our tactical ETF portfolio, we sold Uranium to buy Oil Services, in December. We added credit in the tactical low volatility portfolio and reduced duration, along with foreign exposure.

Rebalancing remains a core pillar of our approach. We believe this disciplined process will serve clients well as markets navigate the next phase, whether that brings continued expansion or new volatility. Staying diversified and risk-aware is the game plan as the economic cycle evolves.

2026 Retirement Contribution Limits

Retirement contributions limits have been announced and raised. To keep our clients up to date, we have released an article highlighting the major points.

Please feel free to reach out with any questions about IRA distributions (including RMDs), taxes, 2026 contributions or just markets in general.

Keep in mind, if you haven't made a Roth contribution for 2025, the deadline for making one is April 15, 2026.

Thanks,

The Friedenthal Financial Team