%20(720%20x%20225).jpg)

More Blog Posts

More Blog PostsApril 2026 - Market Recap

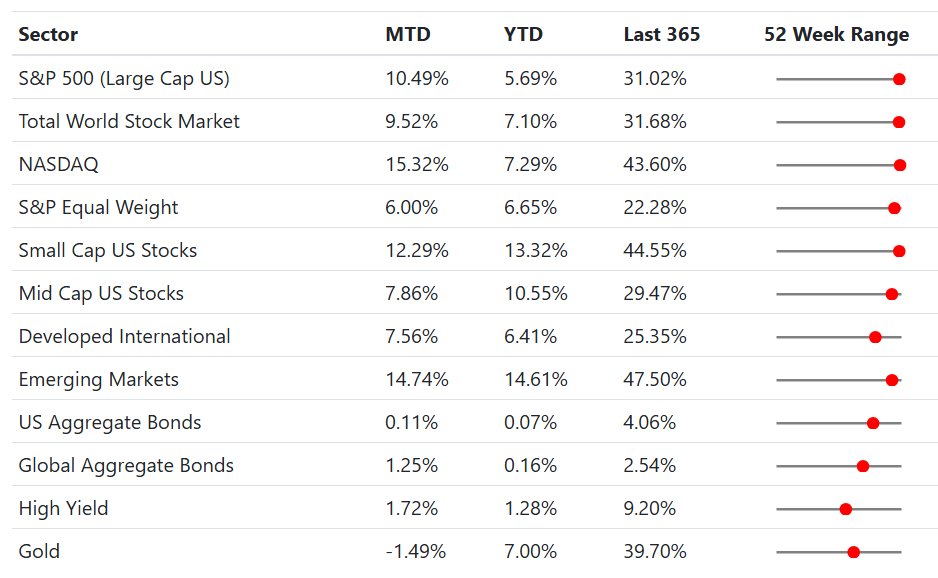

- The S&P 500 gained +10.49% in April, its best single month since November 2020, as a U.S.-Iran ceasefire and a blowout Q1 earnings season combined to reverse March's sharp selloff and push markets to new all-time highs.

- Technology led all sectors with a gain of +20.02%, fueled by exceptional results from Alphabet, Apple, Amazon, and Microsoft. Earnings growth across the technology sector is tracking above 46% year-over-year — well ahead of Wall Street estimates.

- Energy was the only sector to finish in the red, down -2.63%, as crude oil prices pulled back from their conflict-driven peaks following the ceasefire.

- The Federal Reserve held rates steady for a third consecutive meeting and cited elevated energy prices as a reason inflation remains above target. The meeting was unusually divided, with four members dissenting, and it appears to have been Jerome Powell's final meeting as Fed Chair.

Data Dashboard

Stock Market

After a bruising March, April felt like a reset. Two things happened in quick succession that changed the mood: the U.S. and Iran agreed to a ceasefire on April 8, pulling the most acute energy and inflation fears off the table almost overnight, and a Q1 earnings season came in strong enough to remind investors why they own equities in the first place. Neither development was guaranteed. As recently as late March, markets were still pricing in a prolonged conflict and the kind of sustained oil shock that hadn't been seen since 2022. When both risks began to ease at roughly the same time, the resulting rally was broad, swift, and sizeable.

Technology was the clear winner in April, surging +20.02% on the back of better than expected quarterly results. Google's parent company Alphabet's cloud business grew faster than analysts had modeled. Apple delivered its best March quarter in company history. Amazon's cloud unit posted its fastest growth in over three years. What tied these reports together was not just the strength of the numbers but what management teams said about the road ahead: the four largest cloud companies collectively announced capital spending plans approaching $700 billion for 2026, the most ambitious infrastructure buildout the technology industry has ever undertaken. Markets received this mostly well, though not uniformly — Alphabet and Microsoft rose on clear evidence that their AI investment is producing revenue, while Meta fell after raising its spending plans without yet showing the matching payback. That distinction matters. Investors are supportive of AI investment, but they are paying close attention to whether the returns are materializing.

Beyond technology, Real Estate gained +8.74% and Consumer Discretionary rose +8.60%, both sectors that had been weighed down by rate concerns and recession fears through the first quarter and now had room to breathe as the macro picture improved. Industrials were also a quiet standout, up nearly 8%, partly for a reason that connects directly to the AI theme: companies that manufacture the power generation equipment and physical infrastructure that data centers require are running with backlogs they can barely keep up with. Energy was the one sector to pull back, down 2.63% as oil prices eased from their war-driven highs.

April sits squarely in Q1 earnings season, and by most measures this has been one of the better cycles in recent years. More than 90% of S&P 500 companies reporting so far have beaten Wall Street estimates, and the blended earnings growth rate is tracking above 13% year-over-year, the sixth consecutive quarter of double-digit growth. Beyond the headline numbers, what stood out was the tone of corporate commentary. Management teams across sectors described an AI buildout that is creating genuine demand for chips, for power, for physical infrastructure, and a consumer that, while more cautious than a year ago, has not pulled back in any decisive way.

It is worth noting that not all of April's gains were distributed equally. The S&P 500's +10.49% outpaced the equal-weight version of the S&P 500, which gained +6.00%. That gap tells you that large-cap technology names did the heavy lifting for the headline indexes. The good news is that small and mid-cap stocks also posted solid gains, and market breadth improved meaningfully as the month progressed — a healthier sign than a rally that only lives in a handful of mega-cap names.

Emerging Markets were the standout performer in the dashboard, gaining nearly 15% as easing oil prices and improved risk appetite. Developed international markets rose +7.56% as well. Year-to-date, Emerging Markets are now running ahead of the U.S. large-cap index, a rotation that has been building quietly and reflects improving fundamentals in several international markets. Diversification across geographies has earned its keep in 2026.

April Return Summary (by GICS sector)

Bond Market

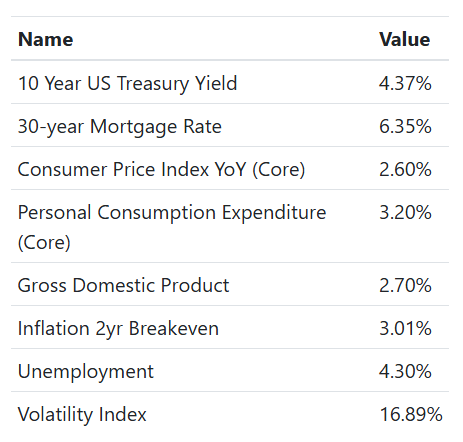

The Fed's April 29 decision to hold rates at 3.50%–3.75% was not a surprise. What caught attention was what happened around the decision. Four FOMC members dissented, the most since 1992, and three of those four were not objecting to the hold itself but to a specific phrase in the policy statement suggesting the next rate move would still be lower. That is a notable shift. It signals that a growing number of Fed officials are no longer comfortable maintaining an easing bias in an environment where inflation remains above target and energy prices are still elevated. Adding to the institutional backdrop, this appears to have been Jerome Powell's final meeting as chair, with Kevin Warsh expected to take over in May.

The 10-year Treasury yield closed April at 4.37%, essentially unchanged from the prior month, suggesting bond markets are comfortable with a prolonged pause.

US Aggregate Bonds and Global Aggregate Bonds both posted modest positive returns in April, a welcome stabilization after the losses they absorbed in March. Yields were largely range-bound, which allowed fixed income investors to collect their income without giving back much in price. After the turbulence of the prior month, a quiet April in bonds was genuinely useful for balanced portfolios.

High yield outperformed investment-grade bonds for the month, as improving sentiment around the ceasefire and strong corporate earnings gave credit investors more confidence in the outlook for corporate borrowers. When the high yield market is relaxed, it generally reinforces what equities are telling us about the economic environment. The two were saying the same thing in April, which adds some credibility to the overall recovery.

Economics

The labor market continues to be a genuine source of reassurance. Unemployment held at 4.3%, and weekly jobless claims in the final week of April fell to their lowest level since 1969. Whatever uncertainty exists at the macro level — energy prices, inflation, geopolitical risk, is not translating into companies letting workers go. A labor market that keeps people employed supports consumer spending, and consumer spending supports the broader economy.

Inflation remains the pressure point. Core CPI is running at 2.6% year-over-year and Core PCE at 3.20%, both above the Fed's 2% target. The 2-year inflation breakeven rate, which captures what markets expect inflation to average over the next two years, sits just above 3%. The energy shock from the conflict contributed meaningfully to headline price pressure, and some of that is now receding as oil prices ease. But core inflation, which excludes food and energy, tells us that not all of the pressure is energy-related.

On housing, mortgage rates edged down to 6.35% from 6.48% in March, a modest improvement that nonetheless leaves affordability stretched for most buyers. High prices and limited inventory continue to keep the housing market subdued. For the broader consumer, the picture is genuinely mixed: households with significant equity and investment portfolios are in good shape, supported by a strong market and rising wages, while middle and lower-income consumers are still absorbing the cumulative effects of several years of elevated prices. The VIX, which we track as a measure of market anxiety, finished April at 16.89, down sharply from 25.25 in March. This reflects how quickly the mood shifted once the ceasefire held and earnings began to land.

Economic Dashboard

Portfolio Changes

In April, our Global Tactical ETF portfolio has benefitted from ~35% exposure to emerging markets. We reduced our metals & mining positions and added Taiwan in our Global Tactical ETF portfolio.

Our Low Vol Tactical portfolio maintains an exposure to global bonds. We also added credit exposure through senior loans.

Please feel free to reach out with any questions about IRA distributions (including RMDs), taxes, 2026 contributions or just markets in general.

Thanks,

The Friedenthal Financial Team